Deep Dive: Fastenal [Part 2]

Deep Dive: Fastenal [Part 2]

Digging into the Numbers

The second part of this deep dive includes the following sections:

Revenue and margin history

Expense management

Capital Intensity

Direct returns to shareholders

Growth plan

Management

Financial Strength

Competitors and Competitive Advantages

Risks

Valuation

Now that we got to know the business in the first part, let’s dig into the numbers:

Revenue and Margins history

After 2 years of slow growth during 2020 and 2021 (mostly attributed to the impact of the pandemic), 2022 reflected a normalization of the business cycle and Fastenal was able to grow their revenue 16% YoY (Price contributed 540 to 570 basis points to growth).

Although the pandemic slowed down sales growth, it wasn’t that much of a big hit to Fastenal, since most of their sales are delivered through their back door. The pandemic also helped Fastenal acquire new customers who weren’t familiar with their capabilities and the quality of their service, mostly from the government and healthcare segment. This helped accelerate growth in 2022 and will most likely continue to be a favorable trend in the coming years.

Fastenal reached important milestones during 2022:

International sales exceeded $1 billion for the first time.

E-commerce sales exceeded $1 billion for the first time.

Net Income exceeded $1 billion for the first time.

Something worth noting is that e-commerce sales surpassed $500 million for the first time in 2020, meaning that Fastenal doubled its e-commerce sales in only 2 years, this is mostly due to the recent changes in Fastenal’s branch model:

“We have altered our branch model in certain respects and that branch model has used to be very much an open showroom for people to come in and buy a lot of product. In many respects, we have reduced the size of that showroom and tried to get a lot of that walk-in business to go online.”

You may have noticed the aggressive decline in GM in 2020 with a slight recovery in 2021 in the chart above. The reason behind this, amongst many other headwinds that presented themselves during the pandemic, was the higher costs of transportation Fastenal had to incur during this period.

During the pandemic, Fastenal experienced higher costs due to a shortage of containers. Not only that, but 35% of containers had to be manually unloaded at the port, loaded on a semi, and driven to Fastenal’s distribution centers. This put a big pressure on costs because putting that product on a semi and driving across North America is a lot more expensive than the container going on a train as it would usually do in previous years. At this time, Fastenal saw a fourfold increase in container cost year-over-year and, if you add the costs of transporting the product on semis, it implied a sixfold increase in costs.

Even through all these headwinds, the Fastenal team managed to aggressively cut costs during the year and grow their OM when compared to 2019, this is a demonstration of the strength that a decentralized culture brings to an organization, allowing them to react quickly to a changing environment, something we will build up on in further detail in the competitive advantages section.

Developments over the past 10 years:

Revenue: 8.6% CAGR.

GM: Has steadily declined from 51.7% to 46%.

OM: Has stayed mostly stable, going from 21.4% to 20.8%.

Let’s dig deeper into each of these developments:

Revenue Growth

Branch revenue has grown at a 3.2% CAGR and Onsite revenue has grown at a 26% CAGR over the past 9 years. As we can see, most of their revenue growth has come from identifying their onsite initiative as a growth driver in 2014.

Branch revenue has grown at a 3.2% CAGR, even while the number of locations has decreased by 5.4% annually.

Most store closures are done when there’s another store in reasonable proximity which can deliver to customers’ sites, and Fastenal is able to maintain 90+% of their previous existing business when they close a store.

Comparatively, onsite revenue has increased at a slower pace than the number of locations (26% vs 28.8%)

Onsites have widely grown as a % of Fastenal’s footprint. In 2015, Onsites constituted 9.1% of Fastenal’s in-market locations; in 2022, they were 49.1%.

Fastenal’s other revenue sources, albeit comparatively small, have also steadily grown in the past 9 years at a 14.4% CAGR. This includes revenue generated outside of their traditional in-market location presence, examples of which include revenues arising from their custom in-house manufacturing, industrial services, leased locker arrangements, and other non-traditional sources of revenue.

The sharp jump in 2020 was due to the effects of the pandemic, one response to which was substantial sales of pandemic-related products that were direct-shipped (versus sold through their in-market locations) as a means of delivering critical supplies more quickly.

Fastenal has enjoyed great growth since its foundation in 1967. One example of this is that, in 2022, the average district manager led a business with annual revenues of $26.9 million.

This means that today, a DM leading an average size district in Fastenal is the “CEO” of a business that is approximately 35% larger than the entire Fastenal organization was when it went public in 1987.

Gross Margin Decline

Fastenal’s gross margin has declined 570 basis points since 2013, this is due mostly to the following trends:

Customer Mix

As Fastenal began dedicating its salesforce energy to seeking bigger customers, national accounts as % of sales have steadily grown over the past years. These customers, due to their scale, have more negotiating power and a broader range of product offerings than smaller customers and therefore have brought gross margins lower.

The average gross margin delta between national account customers and the rest of the business is approximately eight to ten points (!).

Even though management acknowledges that the growth of large customers will put pressure on their GM, they don’t believe this to be something necessarily disastrous for the business, as mentioned by their CEO:

“Gross profit is hit by large accounts. It’s no secret that our growth has been driven by the success we’ve enjoyed in leveraging this network we’ve built into growing a large account business. Because for so many years, most of our growth centered on local customers as we were rolling out our short network. As we’ve developed that store network in the last 15 to 20 years, we’ve very aggressively gone after large account business. We’ve had great success there. That business does not operate at companywide gross margins. But the beauty of going after that business is we can afford to go after that business even with the lower gross profit because that leverages the network we already have in place. And so those growth profit dollars shine right through quite well to the bottom line.”

The CEO expects large accounts to become 70 to 80% of Fastenal’s revenue in the long-term future.

Product Mix

When Fastenal was first born, they were focused solely on selling fasteners. Over time, however, they have vastly expanded their non-fastener product lines. Non-fastener products typically have a lower gross profit percentage than fasteners because in many cases non-fastener products are less technical, have shorter supply chains, and are easier to transport.

The gross margin of Fasteners runs in the 50s, while non-fasteners as a group runs in the 40s. As expected, as non-fasteners products have grown as a % of sales, they have brought Fastenal’s overall GM lower.

In terms of product mix, there’s also a GM difference between Fastener products. For example, OEM Fasteners have a lower GM than Fastenal’s overall GM and MRO Fasteners have a higher GM than Fastenal’s overall GM.

Onsite Growth

Another negative trend is that, as I mentioned in the first part of Fastenal’s deep dive, onsites carry a lower GM profile than branches, therefore onsite growth has also negatively affected its overall GM.

Onsites have a gross margin in the neighborhood of 35%, and an operating margin in the upper teens.

Not only does the onsite have a lower GM in and of itself, but every time Fastenal pulls a customer out of a branch and moves it into an onsite, it temporarily lessens the financial performance of the original branch too, although management likes the trade-off that this implies:

“The trade-off: We ignite the customer relationship, unlock selling energy in the branch, and grow the market faster overall. As you can appreciate, we like the trade-off.”

All of these trends have contributed to the decline of Fastenal’s GM over time and will likely continue to do so in the foreseeable future.

One of the ways Fastenal plans to offset the secular decline in gross margins is by better sourcing and lowering trucking costs.

“Over an extended period of time, we would not be surprised if our gross margins are lower. But that is on the back of significant growth and market share gains.”

—Holden Lewis

Operating Margin

With everything that I mentioned in the previous section, you may now think that Fastenal is heading to its demise. In reality, Fastenal expects its operating margin to stay stable and even expand over time.

“One of the reasons why we're not obsessing over the fact that over a period of time our gross margins are likely to be down is because we do think that the growth initiatives that we have, they may be lower gross margin, but we think they're also inherently easier to leverage. [in terms of operating expenses]”

—Holden Lewis

As mentioned in the quote above, Fastenal has been able to leverage its operating expenses in order to maintain a somewhat stable operating margin.

Another trend that has helped Fastenal’s operating margin is the maturity of its locations. The profitability of an in-market location is affected by the average revenue produced by each site. In any in-market location, certain costs related to growth are at least partly variable, such as employee-related expenses, while others, like rent and utility costs, tend to be fixed.

As a result, it has been shown that as an in-market location increases its sales base over time, it typically will achieve a higher operating profit margin.

The paths to higher operating profit margins are slightly different in a traditional branch versus an Onsite location, as the former will tend to have more fixed costs to leverage, while the latter will tend to have a smaller fixed cost burden but have greater leverage of its employee-related expenses.

In the following quote, the CEO Comments on how expense leverage help offset gross margin headwinds:

“Part of it comes from the inherent leverage that comes in the Fastenal model when the average branch is doing 120 versus 100 [Thousands of sales a month], you pick up hundreds of points of operating margin when it goes from 120 to 150, you pick up expense leverage … a branch doing 100 will lose 100 basis points of gross margin on its journey to 150 a month but it’ll also shed 450 basis points of operating expense and your net win is a 350 point win.”

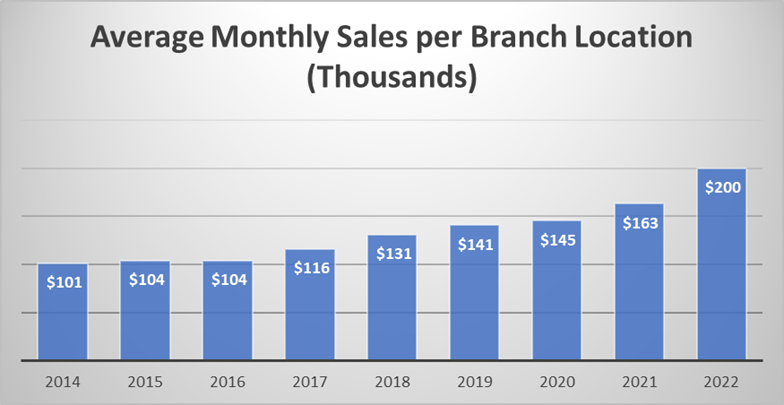

With the addition of so many new locations, Fastenal’s average revenue per Onsite contracted from $158,000 per month in 2014 to $135,000 in 2022. This puts a short-term drag on profitability, returns, and ultimately their ability to produce cash flow. But over time, as this installed base matures, Fastenal should begin seeing its OM slowly expand into the low 20s.

“What I've always said is prior to Onsite becoming an initiative, and we just looked at 215 onsites that have been there, somewhere between 1992 and 2014, they were mature not as a function of time, but a function of scale. On average, those Onsite were doing between $1.8 million and $2 million a year in revenue. And that is when you achieved a margin north of 20% on that group.”

—Holden Lewis

Fastenal’s pathway to profit has changed with the introduction of onsites. Historically, it consisted of growing the average branch size and as that would happen the operating expenses drop dramatically (A branch doing $50,000 to $80,000 a month has operating expenses well into the 30s, while a branch doing $150,000 to $250,000 a month has operating expenses that are well down into the mid if not low 20s).

However, new growth drivers such as onsites have now become a challenge to this previous pathway to profit, since it ends up taking revenue away from branches. This is why Fastenal has been focusing on consolidating branches in most markets, helping bring their average revenue up.

These efforts by the management team will help expand Fastenal’s OM over the long term, even if it experiences some short-term downturns along the way (OM tends to suffer during periods of low-single-digit growth).

In Summary: The business is expected to experience a gross margin secular decline, but they expect to more than make up for it at the operating margin level through SG&A leverage.

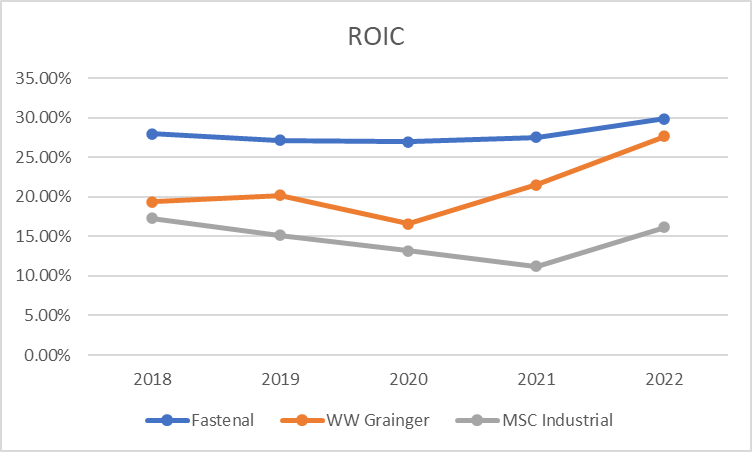

ROIC

Below is a comparison of Fastenal’s ROIC to its two biggest competitors. The industry overall experiences great ROIC (over 10%), but Fastenal is the indisputable leader, with returns that are both higher and more stable.

Expense Management

As mentioned previously, in order to combat its declining Gross Margin, Fastenal has been focusing on finding ways to become more efficient and leverage its operating expenses.

In the last 10 years, SG&A as % of sales has declined by 500 basis points, putting it at a point where it has never been lower in the history of the company, and that’s how the new Fastenal model is supposed to work.

Labor

As a service-based business, most of Fastenal’s expenses are related to labor. Although headcount is an important data point to analyze, what drives most of Fastenal’s employee costs are incentive comps, whether it's in the commissioning in a store or the profit-sharing contribution. It’s not so much about headcount, because headcount adding typically happens a lot at the entry level, which is a lot more manageable.

In the past, they would have had to add a lot of workers to grow their revenues due to their branch-focused model. But today, thanks to their new strategies and technologies there is more leverage in the model for headcount growth than has been the case in the past, as shown below.

Over the last 3 years headcount growth has been allocated as follows:

51% of headcount increase has gone into IT.

35% has gone into either a growth driver, the international team or supporting the sales team.

14% has gone into all other categories combined.

Working Capital

As a distribution business, Fastenal also has to manage its inventory effectively. And rightfully so, the blue team has managed to remove 3 weeks’ worth of inventory in hand from their working capital since Q1 2019, and they believe they can further remove even more weeks from their inventory throughout this year after removing the additional layer of inventory they had to build up due to the disruption of their supply chain during the pandemic.

“When I think of this year, I envision a very, very strong cash flow year, as we saw in the first quarter because we can take not days, but weeks out of our inventory on hand.”

—Daniel Florness, Q1 2023

When it comes to managing working capital and vehicle assets, Fastenal also has its Drive to 35 initiative:

“We have talked internally about what we call our Drive to 35. And what that is, if you look at our internal financial statements … we look at our accounts receivable business unit-by-business unit. We look at fully loaded inventory, that’s local inventory as well as the allocation of distribution inventory. Then we look at our local vehicles. We look at those three assets, and we say an optimal place for us in a $175,000 a month branch, a $200,000 a month branch is 35% of the annual sales.”

Acquisitions

Historically, Fastenal has never been an acquisitive company. In fact, 99.5% of Fastenal’s growth has been organic in the last 50+ years.

Their only recent relevant acquisition was the acquisition of certain assets from Apex Industrial Technologies (Vending partner) for $125 million, and in past years they have acquired some small distributors here and there.

Management usually prefers to invest in their own growth drivers and working capital rather than seek acquisitions:

“When we look at opportunities, that pipeline if you will, we're doing a lot more of evaluating strategic opportunities, rather than simply picking off perhaps struggling competitors as a means of consolidation. That's not the primary focus when we do look into acquisitions. Ours is primarily strategic. So again, at this point, we think a better use of our balance sheet is investing in the working capital that we need to sustain the type of service levels. Which will in turn put pressure on those smaller customers and allow us to gain the market share without having to pay a premium for it.”

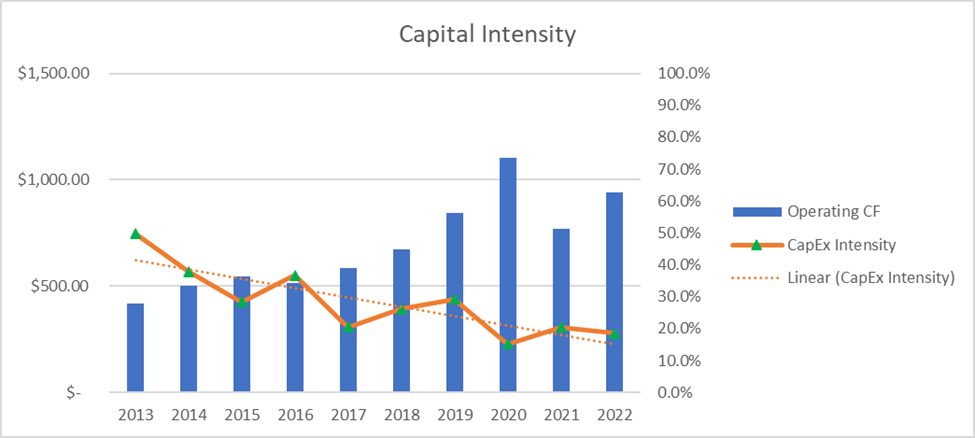

Capital Intensity

Over the past 10 years, Fastenal’s CapEx as a % of their OPCF has steadily declined (Growing onsite locations is a very capital-light endeavor). Most of Fastenal’s capex is dependent on what they are doing in the front of vending, distribution centers and their vehicle fleet.

Management expects net capital expenditures in 2023 to be within a range of $210.0 to $230.0.

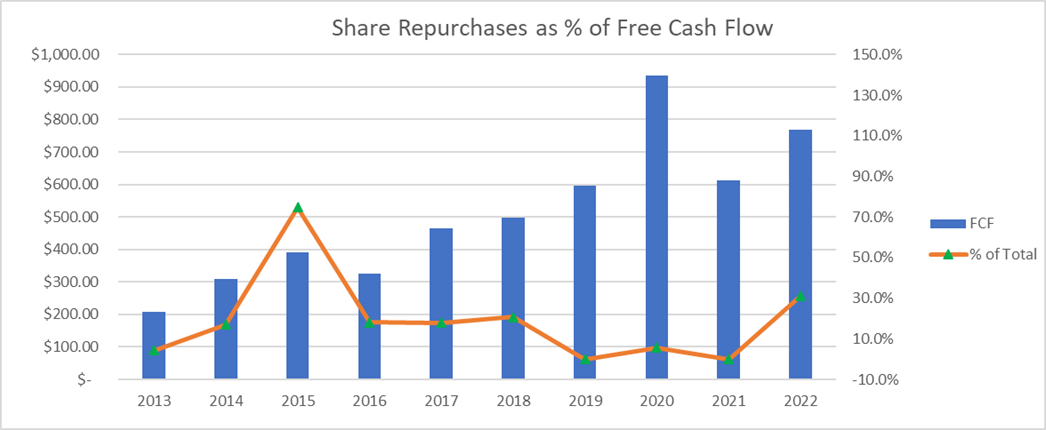

Direct Return to Shareholders

Although Fastenal spends a decent amount of its FCF on share buybacks, due to its compensation plans (which we will discuss below), shares outstanding have stayed mostly flat in the past 10 years, being reduced at a 0.39% annual rate.

I usually prefer to analyze the dividend payout ratio as a % of FCF, but since most of Fastenal’s investments come in the form of working capital I decided to use Net Income in this specific case.

2020 was the third time Fastenal paid a supplemental dividend. The first time was during the financial meltdown late in 2008, the second time was during the chaotic income tax climate late in 2012, and the third time was in late 2020. In all three cases, Fastenal had cash management believed wasn’t needed to fund future growth investments, and felt the responsible action was to return the cash to shareholders

As can be seen above, management returns a lot of its cash to shareholders. They have even borrowed money in the past (2015), to buy back shares (something I’m not really a fan of).

When asked whether they plan on allocating more capital towards dividends or buybacks in the future management gave the following response:

“I think our bias still leads towards the dividend. We have a lot of shareholders that I believe have grown accustomed to that. We have attracted some shareholders because of that aspect of our business, a growth organization over time that pays out a meaningful yield on the stock. Quite frankly, the marketplace has pushed us to buy back some stock by how you price the stock. If our stock had a price that was materially higher than it is today, we won’t be having this discussion, I don’t think. And so, I think the question on allocation in the future is really going to center on where is our valuation. And I don’t mean from an absolute perspective, I mean where our valuation is from a relative perspective, where is our valuation relative to our peers. And the tighter that number is we’re probably more inclined to buy back all the stock.”

Growth Plan

Over its long history, Fastenal’s success in growing has come from being able to gain market share. This is what has allowed it to consistently grow in the cyclical industry it operates in (Since going public, Fastenal’s revenue has only declined once, in 2009).

“We still have incredible opportunities for growth. We have a relatively small market share, and I truly believe, we have a better supply chain model for our customers.”

Historically, Fastenal’s primary growth driver was opening new branch locations. Beginning in the late 1990s, the rate of openings began to slow. By 2007, they had an established footprint in the United States and in Canada; therefore, they slowed their openings further.

The pattern further decelerated to the point where Fastenal had minimal net openings in 2009, and the network began to contract in the 2011 time frame.

This maturation of the branch network gave Fastenal the opportunity to develop and fund new growth drivers, adding new dimensions to their service.

Today, these growth drivers for the long term include:

Expanded national accounts team

Onsites

FMI

International expansion

Let’s dive deeper into each of these:

Large accounts

Large accounts are expected to be one of the main drivers of Fastenal’s long-term growth.

National accounts and government accounts represent just over 50% of Fastenal’s revenue and contribute nearly 70% of their growth

Onsites

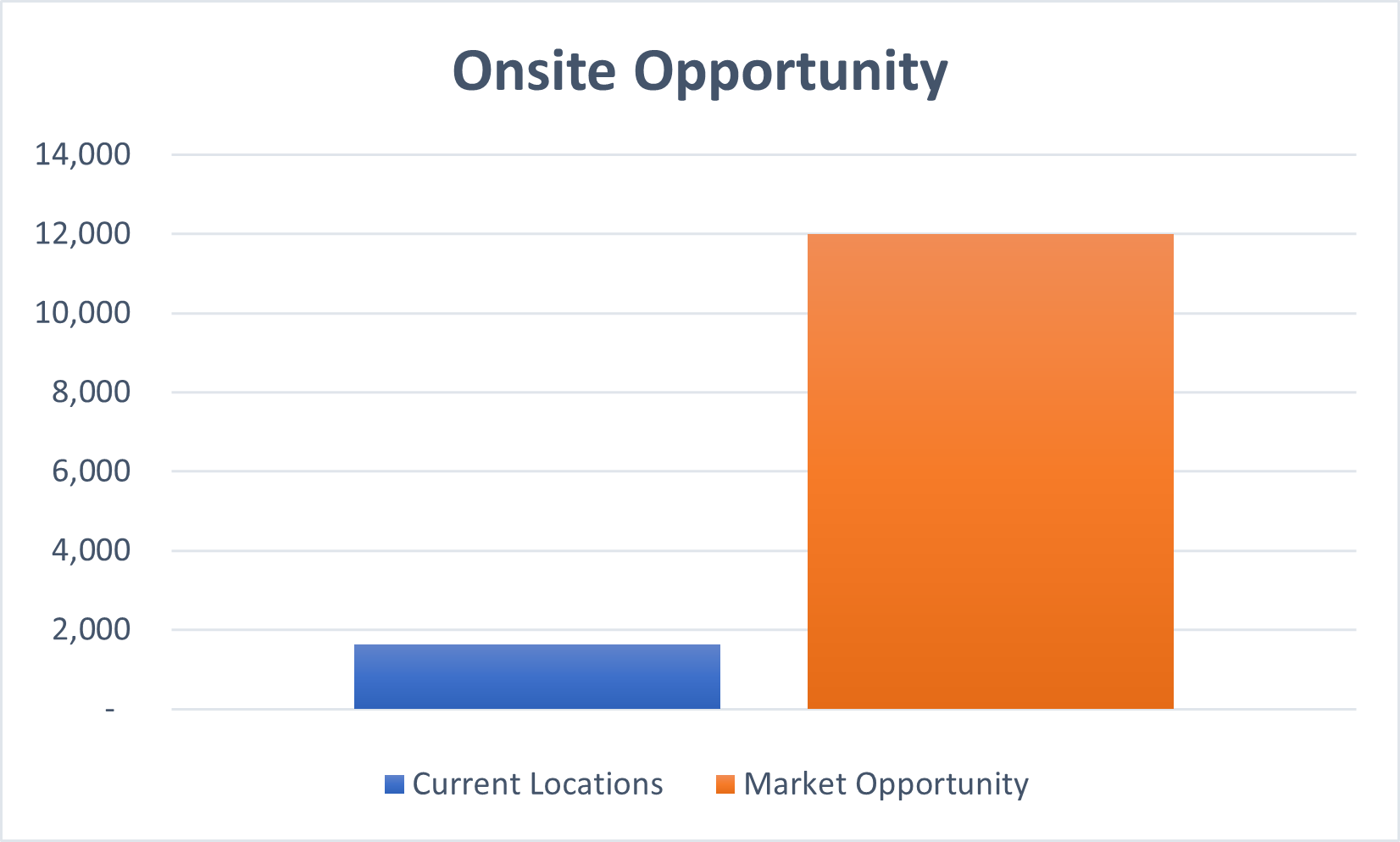

In 2019, Fastenal thought there was an opportunity for up to 4,000 onsite locations. In 2022, however, they identified over 12,000 manufacturing and construction customer locations in North America with the potential to implement the Onsite service model.

Management also believes that as they follow their existing national account customers outside the United States, the market potential for Onsite solutions will continue to expand.

Currently, management believes the marketplace can support 375 to 400 new Onsite signings annually.

In most cases, when an onsite is first implemented, Fastenal takes some sales out of the branch store and that becomes the seed of revenue for that onsite. What they’ve found, is that after 12-14 months that seed of revenue usually grows dramatically from its original number. In many cases, Fastenal has taken a $20k-$30k relationship from a branch and grown it to $120k-$150k in one to two years.

Not only is Fastenal able to grow the initial revenue taken from their branch, but they are also able to strip out a lot of costs once they transition to the onsite model, mostly on the inventory side.

As weird as it may sound, historically, slow environments tend to be favorable for onsite growth, as mentioned by Fastenal’s CFO:

“[The following statements refer to customers, not Fastenal] If you are in an environment that’s either cascading lower or cascading higher and your energy in an organization is being spent on managing those inflections and those significant changes, then your ability to spend a lot of energy on an implementation process becomes a challenge. So that would probably suggest that there’s a great case to be made for onsites when people are trying to be cost-conscious and working capital conscious and that certainly is the case in a downturn. But it would depend on the magnitude of what you are talking about. I would say in a modest downturn, we probably are in a better position to be able to sell what we do. If you have a dramatic growth or dramatic downturns, I think, that our customer’s energy can be moved into other things.”

Another great benefit of onsites is that, in most cases even if Fastenal is unsuccessful in implementing the model with a customer, they are usually bringing back more revenue to the branch than they initially took once a closure is made.

FMI

Fastenal’s bin and vending initiatives have been another great source of growth for Fastenal in the past and will continue to be one of their main growth drivers.

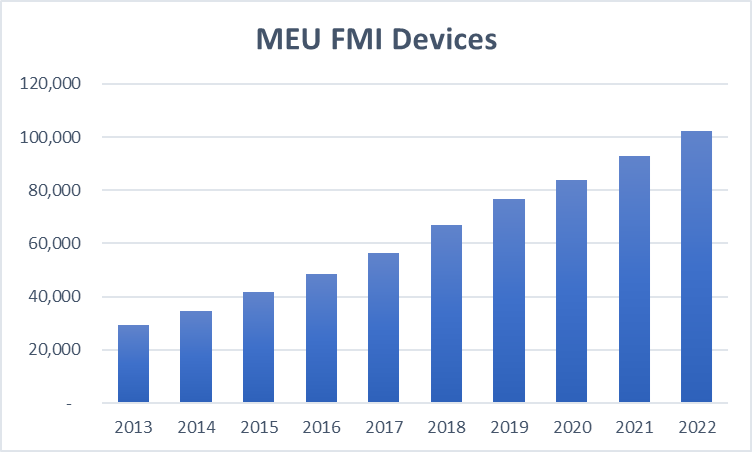

Fastenal’s MEU FMI installed base has experienced an 18.6% CAGR over the past 10 years.

Fastenal reports their FMI devices as “machine equivalent units” (MEUs). This conversion takes the targeted monthly throughput of each FMI device installed and compares it to the $2,000 target monthly throughput of their FAST 5000 vending device.

For example, an RFID enclosure, with a target monthly revenue of $2,000 would be counted as a '1.00' machine equivalent. An infrared bin, with a target monthly revenue of $40, would be counted as a '0.02' machine equivalent ($40/$2,000 = 0.02).

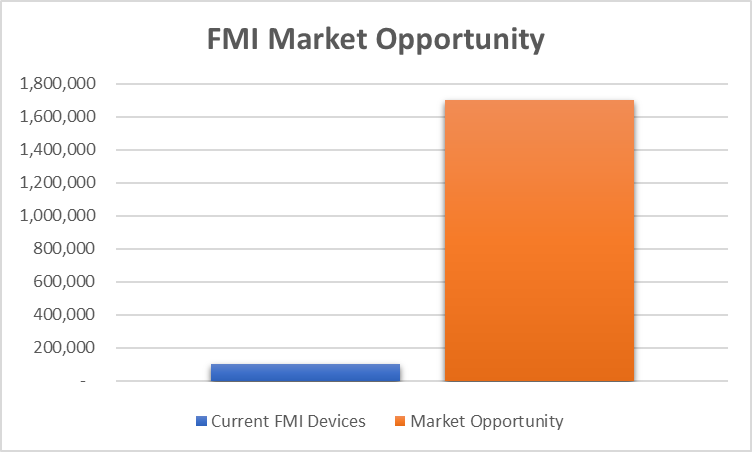

Management currently estimates the market could support as many as 1.7 million vending units and, as a result, they anticipate continued growth in installed devices over time.

Target monthly revenues per vending device typically range from under $1,000 to more than $3,000.

Not only has FASTVend experienced rapid growth in recent years, but Fastenal has also managed to expand the margins of this initiative. Five years ago, the vending initiative had operating margins between 13% and 14%.

After discussing with the vending leader, the CEO realized they needed to work on:

Increasing revenue per machine.

Increasing the mix of Fastenal’s exclusive brands.

Increasing the mix of Fastenal’s preferred providing brands.

Lowering the cost of devices.

Now that all of these have been implemented, as of 2022, the vending segment broke the 20% mark for its operating margin for the first time.

FASTBin has also been gaining a lot of strength. A couple of years ago, if you looked at the discrete number of FMI signings per day, one of those signings was a FASTBin, today, it’s 15. This demonstrates that this initiative is rapidly growing throughout the organization and customers are embracing the technology.

International Expansion

In 2022, the North American region accounted for 24.2% of the global revenue share of the industrial fastener market. With almost 97% of Fastenal’s sales coming from NA, it is evident that the international opportunity is substantial, but their speed will be limited by their relatively underdeveloped infrastructure in comparison to the United States.

Another great difficulty for International Expansion is that Fastenal is not as well recognized outside of the U.S. and Canada, which hinders their ability to sign business deals that are not related to the foreign operations of their NA customers. So far, though, it seems like Fastenal is being somewhat successful in gaining a reputation outside of NA, as mentioned below:

“You're seeing examples of customers we're signing and onsites we're signing or branches that customers that we’re creating relationships with that aren't strictly an extension of North America. There are businesses we're signing up contracts with that know nothing about our business in the U.S. or our business in Canada, or our business in Mexico … That's the exciting part because it tells me the team is creating a market presence for themselves and they're being recognized in the supplier community.”

Management expects significant growth in the next 5-10 years to mostly come from NA as has been the case in the past, since as they mention below, the growth opportunity there is still significant:

“We believe we have a significant opportunity for growth based on our belief that North American market demand for industrial supplies is estimated to exceed $140 billion.”

But going further than that they’ll have to expand internationally at some point if they don’t want their growth to stagnate. Not only will this expansion require a significant amount of capital and time, but it could become another headwind for the business’ margins due to the lack of scale and density of the distribution network they would initially have in these areas.

Jeff Watts (EVP of international sales) expects international sales to reach the $6 billion dollar mark in under 10 years. I believe this to be quite an optimistic target, but Fastenal has a great decentralized team and perhaps they’ll be able to execute properly and reach this goal.

Fastenal as a $10 billion business

Fastenal is very quick to remove its old shareholder meetings, therefore I had to borrow the following picture from one of YoungHamilton’s articles. He has a great Substack and I highly encourage you to check his posts out if you haven’t yet.

In its 2019 meeting, management pictured how Fastenal would look as a $10 billion business. I assume that it would take Fastenal about 5 years to reach that number taking into account historical growth numbers, and there are a few things we can infer from this image:

International sales still won’t be an extremely relevant part of Fastenal’s business, representing 13% of total sales.

The product mix will be 75% non-fasteners and 25% fasteners (compared to a 66-34 split as of 2022). This seems very feasible since non-fasteners have historically grown about three percentage points faster than fasteners.

Onsites and vending devices will continue to experience great growth in this assumed 5-year period.

The average revenue per site will continue to trend up, helping combat the gross margin headwinds from product and customer mix (something we’ve covered extensively already).

In another more recent meeting, management pictured Fastenal both as a $10 and $15 billion business. Over time, they expect their operating margin to expand up to 22% and for net capital expenditures to hover in the 3% range. They also expect that their Drive to 35 initiative will be successful, which as we mentioned before, implies that their working capital will represent 35% of sales.

“There's been no change in our expectation that we're going to be a 20% to 22% operating margin business and a 25% plus return on capital business.”

—Holden Lewis, CFO

Management

Some of the main characteristics I like to analyze when it comes to management teams are:

Their behavior (Integrity, trustworthiness).

Their ability to execute.

Having a long-term view.

Fortunately, Fastenal’s management checks all the boxes. When things aren’t going great in the organization, the CEO is quick to take accountability:

“We moved a bit too slowly on challenging our gross profit margins. As president and CEO, that’s on me.”

“I think there's a bit of fatigue in the organization from all the tariffs and pricing and inflation energy that we have expelled in the in the summer and fall months. And I think it showed up in our fourth quarter. That's an execution issue on Fastenal and that's on me.”

The CEO has also demonstrated to have a long-term view:

“We limit our priorities to just four things: our customers, our employees, our suppliers, and our shareholders … We approach these four priorities with a long-term perspective and a ‘short-term edge …. That said, we sincerely hope you view Fastenal as a long-term investment, not a short-term rental – this ensures our goals are aligned.”

“One of the things that I believe it’s important to our business today is that every day you rationalize your business with a view towards five to 10 years from now.”

In another meeting, management also mentioned that they constantly ask themselves: “What financial performance must we produce to attract long-term investors to Fastenal?”

Another aspect I like about the management team is that they’re not the type of people to fall for the trap of thinking they can predict what the economy is going to do:

“I suspect for most people listening to this call, the reason you're looking at our earnings release today and looking at participating in this call is you want to see what breadcrumbs might come out of it as far as where the economy is going. Spoiler alert, we've often said that our visibility to the future is about 8 hours.”

“We’ve never been good at forecasting the future, so we’ve tended to stay away from it.”

Also, not only does Fastenal’s CEO write a letter to shareholders every year, but he also writes a letter to employees. In it, he communicates about important events, milestones and asks them for suggestions.

We can thank Fastenal’s great culture and quality of leadership to its founder, Bob Kierlin, which made to sure to instill his great values in the organization he built

Fastenal has a big focus on developing great leaders inside their organization, which they train through the courses in their “Fastenal School of Business”. Their biggest pipeline of talent over the last 50 years has been reaching up to students with one to two years left of college, and offering them a part-time job, with the hopes that when they graduate, they decide to come work full time for them. After the hiring, they put a lot of effort (and money) into training these individuals.

This method to acquire employees, paired with their promotion-from-within culture, leads to Fastenal having a CEO that has been a member of the organization since 1996 and executives that have been part of the blue team since the late 80s.

Compensation

Another aspect I like to analyze when it comes to management is how they’re compensated.

“Never, ever, think about something else when you should be thinking about the power of incentives”

—Charlie Munger

Employees

In the case of Fastenal, not only do top executives get compensated for sales and gross profit growth, but people at the branch, support, and distribution levels throughout the organization also have incentive comps.

“We believe it is harder to grow than it is to maintain. We pay a higher commission on growth. Just like we pay a higher bonus to our non-sales personnel on profit growth than on profit. Because status quo is easier than change. And we reward for change.”

Approximately 71% of employees have a job related to sales. They are offered a major opportunity to earn bonuses, paid monthly, based on growth in sales, gross profit achieved, the opening of new accounts, increase in sales to active accounts, prudent management of inventory levels, and collections of accounts receivable.

The remaining 29% are similarly compensated for their contribution to attaining predetermined departmental or project and cost containment goals, mostly focused on either customer service or better execution of company-wide activities.

Executives

Fastenal’s executive compensation is quite simple, everyone but the CFO gets compensated based on pre-tax earnings growth of the company and/or their area of responsibility, while the CFO gets compensated based on company-wide net earnings.

NEOs are also eligible for a supplemental bonus program, known as the ROA (Return on Assets) Plan, which is intended to encourage better management of accounts receivable, inventory, and vehicles and provides cash incentive amounts on a quarterly basis for asset management improvement over the same quarter in the prior fiscal year.

NEOs bonuses are paid in cash on a quarterly basis when Fastenal exceeds 100% of pre-tax earnings (or, for the CFO, net earnings) for the comparable quarter of the previous year. These cash incentive bonuses are determined by applying a payout percentage to the amount by which pre-tax earnings or net earnings exceeded 100% of pre-tax earnings or net earnings for the same quarter in the previous year.

The main principles behind Fastenal’s compensation philosophy are the following:

Annual base salaries are generally below the market median.

Quarterly cash incentive opportunities are typically above the market median.

Vesting periods for equity-based compensation are longer than typical in order to encourage long-term perspectives among employees.

Focusing on quarterly growth in profits provides executives with the immediate feedback necessary to take prompt action to correct unacceptable financial results, and the motivation to take such action.

By using actual profits in previous periods, rather than projected profits, as the basis for setting the minimum performance targets in future periods, Fastenal reduces the incentive to manipulate results. As any overstated profits giving rise to increased bonuses in one year would result in overstated minimum targets, leading to reduced bonuses in the next year.

By having base salaries below average and compensation above average, Fastenal makes sure that the actions of its executives are motivated by the desire to deliver superior results.

They also have systems in place that let their employees know, on a daily basis, how their business is performing compared to other businesses within the organization and how that performance impacts their compensation.

They also pay cash bonuses as close as they can to the time when the work is performed and results are achieved, as opposed to waiting until the end of the year, or several years.

“We believe that quick payment of cash bonuses serves to motivate our people and limit business risk.”

Fastenal also has guidelines in place that require directors and executives to hold a minimum amount of equity. In all honesty, I find these to be somewhat low compared to what I’ve seen in other businesses, but they’re better than nothing.

Financial Strength

I won’t go into much detail here since Fastenal’s balance sheet is extremely conservative. Their LT Debt / FCF ratio is less than 1, and their debt calendar doesn’t pose a threat at all.

Competitors and Competitive Advantages

Fastenal’s top two competitors are WW Grainger and MSC Industrial. Fastenal’s and MSC’s end-market distributions are very similar, with 70%+ of sales coming from manufacturing. Grainger, on the other side, is not as concentrated in the manufacturing market, with only 31% of its sales coming from it.

Besides these two main competitors, the MRO market also has seen the appearance of many e-commerce-focused players, such as McMaster & Amazon. Amazon acquired smallparts.com in 2005 and rebranded it to Amazon Supply in 2012. Amazon then relaunched this segment in 2015 as Amazon Business. Today, Amazon has many customers that shop on Amazon Business and its prices are lower than many of the large distributors, even those that have focused on building a price-competitive online presence.

While most competitors such as W.W. Grainger decided to compete with Amazon on price and selection, Fastenal took a different route. Instead of competing on price or selection, Fastenal decided to get closer to the end customer by increasing the number of onsite and vending locations.

Fastenal utilizes almost 9x the locations of Grainger to generate 45% of their level of sales. Similarly, it has 61x the locations of MSC Industrial and generates 2x their sales. With this data alone, most people would assume that Fastenal has lower returns than its competitors, but as we’ve seen in the comparison above, this is not quite the case.

Although the MRO market may have a commoditized nature, what Fastenal offers its customers is more than just a supply of products, they help them free up resources and make their operations more efficient.

"Our customers today are asking us to create more value for their business. And they're asking us to create that value through managing their supply chain. So I'm going to talk about really what does that mean. So I brought a prop with me today. And this is a Zinc-plated Grade 5 Hex Cap Screw. It's one of the fastest-moving parts we sell in Fastenal. If you go on our website today, the bolt sells for $0.43 … managing the supply chain for this $0.43 bolt is complex, surprisingly complex. It's not a core competency for our customers. It is a core competency for Fastenal. So more and more, our customers are asking us to create value for their business by managing this bolt along with tens of thousands of other SKUs. What do they expect when they ask us to manage this bolt? They expect us to have it at their facility on time when they need it. They expect us to deliver a bolt that meets their quality standards. Those are just table stakes. They expect a lot more than that. They expect us to free up their working capital. They expect us to lower their expenses. They expect us to improve their P&L, increase their quality, increase their production, impact their capacity and lead times and to improve their worker and end-user satisfaction. Those are a lot of expectations for a $0.43 bolt."

As an example of what Fastenal does for its customers, they obtained the following stats through customer site evaluations (2018-2020)

55% average reduction in material distribution hours. (Allowing the business’ employees to focus on other activities)

37% average reduction in inventory value. (Allowing the business to free up working capital for their investments)

36% average reduction in employee travel time.

“Once we finish a customer’s facilities analysis, there are very few companies, if any that can compete with our systems, our efficiencies, our speed to implementation and more importantly the value and cost savings that we can provide.”

So then, what leads to Fastenal’s superior returns?

Trucking Fleet

As opposed to its two biggest competitors, which rely on third-party logistics, Fastenal decided to build up its own captive fleet.

Management estimates that the company saves about $100M in costs by operating its own fleet, and it also gives them better control over their distribution.

This fleet is especially advantageous in aggressively inflationary environments, such as the ones we experienced in recent years, where with fuel costs going up, companies relying on 3PL see their transportation costs tick up at a much higher pace than Fastenal.

And why is this important? For fastener products, no more than 1/3 of the value of a fastener is the actual raw material itself. The rest of it is value-added, manufacturing and transportation costs. This means that whoever is able to optimize these operating costs to a bigger extent will enjoy higher margins, and as we’ve already seen, Fastenal has the lead there.

Another way that Fastenal takes advantage of its fleet is by backhauling from its suppliers and more recently from some customers. They often reach out to one of their Onsite customers and say: “You got some pallets you need moved? We’ll move it for you.”

Not only does Fastenal’s fleet help them in terms of costs, but it also allows them to offer to provide a quality of service that is very different from their competitors:

“A year from now, I fully expect us to be able to take an order from a customer that comes in late in a day, maybe in the evening. And let’s say one time in a hundred that customer is in a jam and they need it like two hours ago. Our competitors are probably going to freight that in using small parcels and it’s not getting there till 10 o’clock tomorrow morning, and that’s a really expensive trip. Our driver gets to that branch at 4:00 in the morning or 6:00 in the morning. You pick enough of the time, because it’s different for each branch. Our driver could throw that item in an outdoor locker and that customer gets a text at 4:00 in the morning to the item you ordered at 5 o’clock last night is here, and nobody else in that market can do that. So to me, the value of a captive trucking is you can provide a level of service that just separates you in the marketplace.”

—Daniel Florness

Proximity to Customers

One of Fastenal’s guiding principles is that they can improve their service by getting closer to customers, and this is what they’ve focused on doing in the last decade. Their most recent growth drivers such as FMI and onsites offer significant value by providing a differentiated and “stickier” service than a conventional retail store model.

The advantages of onsite locations include:

Less investment is required, as Fastenal does not need to lease/buy any physical space since they’re getting installed inside their customers’ facilities

They are more capital-efficient as the inventory stocked is site-specific leading to lower inventory needs and better inventory turns.

They offer substantial revenue growth opportunities with large customers. If a customer is already buying fasteners from them, for example, Fastenal can offer the prospect of also supplying and managing their MRO supplies.

Once the location is established, Fastenal becomes entrenched in the customer’s operations. They manage their working capital, and Fastenal’s employees become part of the customer’s team.

Another advantage that the FMI and Onsite initiatives bring to Fastenal, is that not only do they allow it to add value to customers through data (which leads to more efficiency), but that it also ensures that Fastenal always has a reason to be in the customer’s facilities. The blue team employees are always there either refilling FMI devices or managing the onsite, which allows them to approach the customer and look for opportunities to gain more business.

This is very different from an e-commerce-focused or branch-driven model, where you would have to gain entrance into the customer’s site.

The model Fastenal has adopted should allow them to become more resilient and less vulnerable to distributors focused on e-commerce than their competitors which operate a more capital-light model. This should translate into higher returns for a longer period of time.

“If you think about our value prop … It’s always been about getting really well-trained people close to the customer and empowering them to make great decisions to solve customer issues”

Culture

We can thank Fastenal’s great operational culture to its founder, Bob Kierlin, who made sure to ingrain several principles in the organization’s employment philosophy:

Decentralization: placing employees close to their customers' operations and trusting these employees to independently make local decisions to provide differentiated local service.

They are a passionately promote-from-within company, guided by a belief that if you work hard, make great decisions, learn from mistakes, and exemplify their cultural values, you should receive greater opportunity and responsibility.

A frugal culture, allowing them to be profitable where other competitors can’t.

When it comes to decentralization, by giving people the freedom to make decisions at a local level, Fastenal is able to move faster than its competitors, since everybody isn’t looking for somebody else to tell them what to do.

“We are a decentralized company with decisions made by those closest to our customers. We minimize central planning as we believe it stifles the creativity of our people and because it is, quite frankly, too slow.”

Another value that Kierlin instilled in Fastenal is having a frugal culture. In 1997, he won the title of the cheapest CEO, where the magazine said “Fastenal … is to cheapness what Michael Jordan is to basketball: the best ever.”

As Fastenal’s CEO, he took home the same $120,000 yearly paycheck for a decade, even though the Fastenal board had repeatedly authorized an increase for him. His office, just like most of the organization’s offices, was full of used furniture and he didn’t have a personal secretary.

“And then there are his suits. At a discount store, they'd probably go for $200 apiece. But Kierlin didn't buy them there. He got them from the manager of a men's clothing store. Not from the manager's store. From the manager. The suits are used. "Luckily, we're the same size," says Kierlin, a triumphant smile crossing his face. "I picked up six of those suits for 60 bucks each."

Also, as they do today, Fastenal took advantage of their pickup trucks to backhaul other companies’ goods while making deliveries, helping them save over $100,000 each month.

A big demonstration of their promotion-from-within culture can be found in this article from 1997 too. At the time it was published, Will Oberton was Fastenal’s vice president and later became CEO from 2002 to 2014. Daniel Florness was Fastenal’s CFO at the time and then became CEO in 2016.

Going back to frugality, the Fastenal team always embraced this attitude, since they realize that cheapness helps the bottom line, which fattens paychecks. By keeping operating costs very low, Fastenal can pay their employees incrementally higher wages through their compensation plans, and thus more effectively develop and retain talented salespeople.

It is more than obvious, though, that a company cannot survive on cheapness alone. Without good products, marketing, and distribution, cheapness means little. But the good news is that Fastenal also has all of these other qualities, meaning that cheapness gives them an extra edge.

"Frugality is an attitude you develop," Kierlin says. "Once you have it, it sticks with you in everything in life. You don't have to think about it."

This frugal culture, and the ability to operate efficiently together, has been made easier by Fastenal’s historical ability to grow organically. Organic growers don’t operate with a multitude of computer systems and conflicting business cultures. Every employee grew up on the same Blue Team and therefore shares the same values and goals.

Distribution Network

Despite the commoditized nature of most of Fastenal’s products, their distribution is complex, especially that of fasteners. This is in part due to the very high weight-to-value ratio of the product.

Fasteners are heavy and expensive to ship and they don’t cost very much, which means that Fastenal gets a big cost advantage from having lots of stores close to its customers

The proximity to customers that comes from Fastenal’s extensive distribution network also means that Fastenal usually has a quicker delivery time than competitors, which is another big advantage given that manufacturers typically need fasteners when something breaks, and with downtimes being so expensive, this is something customers want to avoid at all costs.

Another layer of complexity comes from the tremendous variability among fastener products, where the supplier has to appropriately stock hundreds or even thousands of SKUs in the right place and at the right time to avoid working capital requirements creating a drag on returns.

Fastenal has spent almost 60 years perfecting the art of effectively managing its complex supply chain. And today, the company’s scale, owned distribution network and collective customer data have helped it obtain both costs and service advantages in its product distribution.

Other strengths that Fastenal has include:

A resilient operating model that assures that customers will always have what they need, even if it comes at a cost to them:

“Being at an organization that has months of inventory on hand because of our network and how we operate while it’s an expensive way to operate, it’s also an incredibly resilient way to operate. I think that has shined through in the years past when there was a little bit of chaos going on in the supply chain. It allows us to be a little bit more agile because we do have some inventory on the shelf.”

—Holden Lewis

Switching costs in the fastener segment:

“The beauty of that business is incredibly sticky. It’s really invasive and complicated and painful to switch a fastener supplier. Because that’s a very tight relationship because I’m supplying you the stuff you need in what you’re producing and the quality, the source supply, all those things we bring to the table are critical and it’s very, very disruptive to change your supplier.”

To summarize

“We believe our success can be attributed to our ability to offer customers a full line of quality products, our convenient locations and diverse methods of providing those products, and the superior service orientation and expertise of our employees.”

Risks

Reliance on suppliers from Asia: Most of Fastenal’s products are bought from China, Taiwan, South Korea and other foreign countries. A disruption in these sources of supplies, either from regulations or unfavorable trade relationships between the US and these countries could affect the business’s ability to obtain the products it needs. This is an important risk because, for both fasteners and non-fasteners, there is not enough capacity to handle it domestically. This means that even if Fastenal wanted to source its products from the US it wouldn’t be able to fulfill its customers’ needs.

Fun fact: 52% of the steel that’s produced on planet Earth is produced in China.

The introduction of new tariffs, such as the ones the industry experienced in 2018 (232 and 301), could make sourcing products from overseas more difficult and/or more costly, which would adversely affect the business’ margins.

Valuation

Now that we’ve thoroughly studied this business, it’s time for the final step, valuation.

Although the market may do very irrational things at times, in the case of Fastenal it has done a nice job of identifying the quality of Fastenal’s business, and therefore it has assigned a notable premium to it related to the overall industry.

Even the management team is aware of this, as shown in the following quote:

“Historically, investors have given our earnings a higher multiple, or premium, than is typical of the broader industrial sector of which we are typically associated. We believe we have earned this premium by virtue of a long history of superior growth, profitability, and returns.”

As of the day of this writing, FAST 0.00%↑ trades at a price of ∼$57 a share.

Note: Historically the board has made a decision to split the stock once the $60 price mark is reached, so we may see a stock split soon. (Random comment, not necessarily a prediction, and not that it makes any difference)

Performing a reverse DCF and assuming a yearly buyback rate of 1%, Fastenal would have to grow its FCF at a yearly rate of 10% for the next 10 years in order to meet my desired RoR of 10% (excluding dividends).

I don’t find this level of growth to be extremely unreasonable, but I don’t find it to be conservative either. I would consider a more reasonable range of growth to be in the 7-8% realm.

As I typically do in these cases, I will be adding this great business to my watchlist and wait for Mr. Market to bring me a buying opportunity in the future.

Closing

And that’s all from me today! I hope you found this post valuable, and if you did, I would greatly appreciate it if you could share it in the button below.

If you are interested in long-term investing & market psychology, you can subscribe to this newsletter, where you’ll receive articles sharing valuable insights on these topics for free.

And you can also follow me on Twitter, where I share short-form content on a daily basis, including a weekly thread and quotes from great investors.