The second part of this deep dive includes the following sections:

Revenue and margin history

Expense management

Capital Intensity

Direct returns to shareholders

Growth plan

Management

Financial Strength

Competitors and Competitive Advantages

Risks

Now that we got to know the business in the first part, let’s dig into the numbers:

Quick Note: Numbers included in this deep dive are in US Dollars unless otherwise stated.

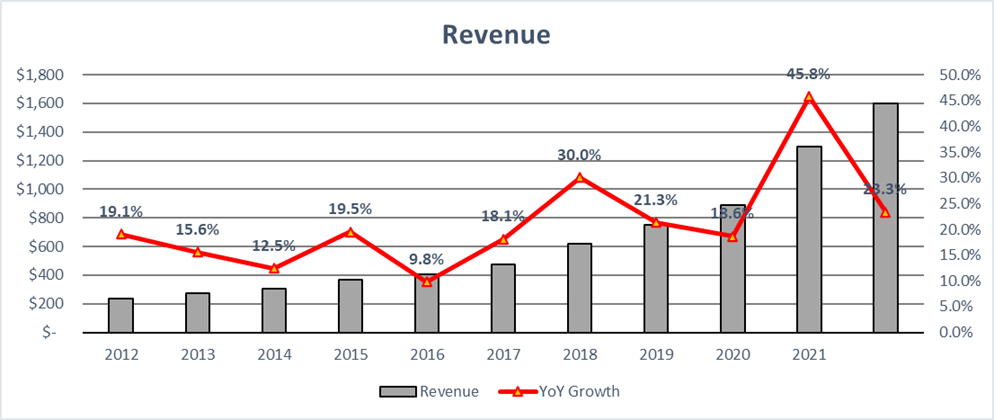

Revenue history

Over the past 10 years, Fox’s revenue has grown at a CAGR of 21.1%. Part of this success has been attributable to the growth of the high-end bike industry and the success Fox has had in the powered vehicle business, with various OEM wins (which we will cover shortly) and continued success in the aftermarket.

After experiencing some headwinds in 2020 due to the pandemic, where Fox had to operate with limited production and OEMs’ factories in the US were shut down, the company’s sales exploded, growing 80% in just two years.

With consumers staying at home, having a lot of free time and traveling being restricted, most people turned to mountain biking and off-road activities to spend their leisure time, benefiting Fox’s top line.

It is important to note that these recent levels of growth are not sustainable, with management guiding for $1,700 million of revenue in 2023, a 6% YoY change.

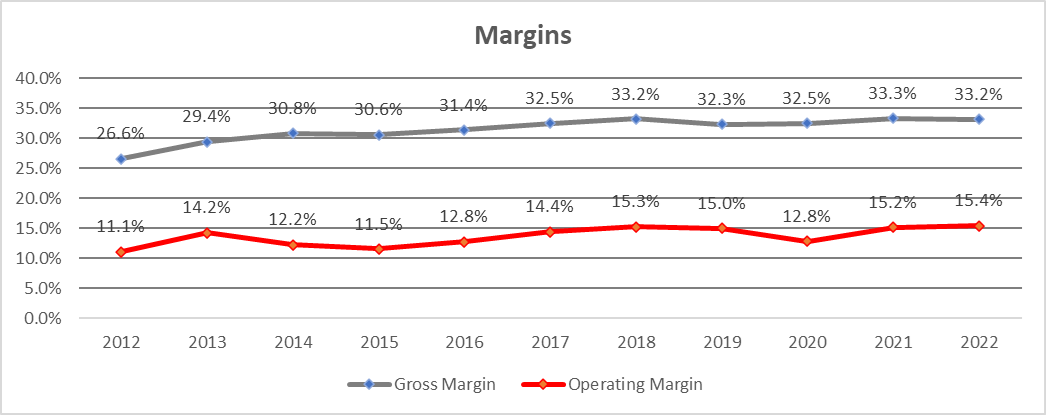

Margins history

The company’s margins have considerably increased over the past 10 years, with GM expanding by 660 bps and OM expanding by 430 bps.

The main variables that drive Fox’s margins are:

Customer Size: The bigger the customers, the lower the margins.

Channel: Margins in the aftermarket are higher than those of OEM customers.

Business group: In the aftermarket, specifically, margins are higher in the bike business than in the powered vehicle business. This is because Fox acts as its own distributor and dealer in the US bike business, while it always has to go through distribution for its PVG aftermarket sales.

Product price point: The higher the price point, the higher the margins.

Note: Although the upfitting business has higher gross margins, it can have considerable OpEx with its commission structure, leading to lower operating margins.

Note 2: It is important to note that a higher GM with a customer won’t always directly translate to higher operating margins. This is because, depending on the customer’s SKU count, Fox might have to incur lower or higher R&D costs to support that customer in particular.

These are some relevant events we can pinpoint in the previous graph:

GM Decline in 2019-20: Due to the effects of the pandemic, Fox experienced various supply chain inefficiencies caused both by outsized demand and troubles with suppliers, leading to material increases in input costs.

OM Decline in 2019-20: Similarly, Fox experienced various pandemic-related costs in its factories due to COVID cases and labor stoppages, where it was basically paying its employees to stay at home.

As we covered in the first part of this deep dive, the OEM business has continually grown as a % of Fox’s sales, and yet, the company’s gross margins have continued to expand. The reasons behind this are two important changes the company made at the manufacturing level:

Moving SSG production to Taiwan

Fox began the transition of 85% of its SSG manufacturing from California to Taiwan back in 2014, with the remaining 15% being left in the US to support local customers. This was a drag to the company’s margins at first, however, once the transition was completed, it became the main reason behind Fox’s margin expansion from 2015 to 2018 due to:

Reduced production lead times.

Reduced manufacturing costs.

Shortening of the supply chain.

Move from California to Georgia

Once the company fully benefited from moving SSG manufacturing to Taiwan, it then decided to move its PVG manufacturing from California to Georgia in the middle of 2019. Although the differential in labor and other costs from California to Taiwan is much greater than the differential between different parts of the US, Fox still expects to benefit from a GM improvement of 250-350 bps for that part of the PVG business.

After various inefficiencies from the initial ramp-up and duplicative costs during the first stages of the transition, the benefits began hitting the P&L in 2023 Q1.

Something important to note, and the main reason behind the initial inefficiencies of this transition, is that it takes about 4-6 months for a product line to be mature enough to overcome the lower quality levels of new employees. Since Fox launched a lot of products in 2022 at the new facility, these are now running in core production mode in 2023.

Further, management expects that as the business continues to grow its volume in PVG, Fox has another 200-300 bps opportunity for GM improvement ahead of it. This is expected to happen in a non-linear manner over the next 12-18 months.

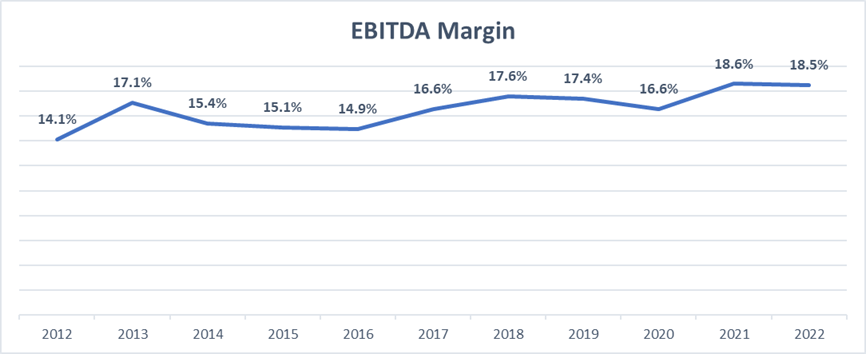

EBITDA Margin

Although it is a metric we don’t usually pay attention to, management has stated many times that they prefer to focus on EBITDA margin over GM. Fox’s EBITDA margin has expanded by 440 bps over the past 10 years.

The company’s long-term goal is to get its EBITDA margin to the 20%+ level.

Business segments

SSG

Fox decided to change the name of its bike segment to specialty group in 2018, as it looked to expand beyond things that go directly on a bicycle toward things that could get sold to that same passionate customer base. The company recently acquired a mountain biking footwear company in 2023, so this might be what they were referring to.

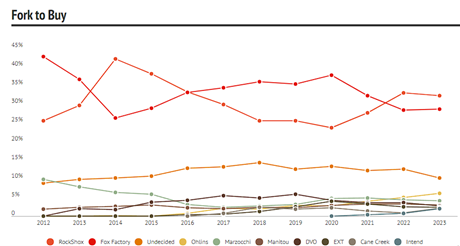

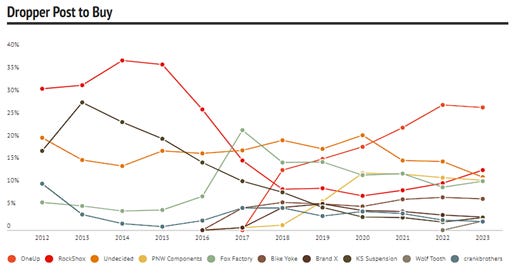

SSG sales have grown at a 15.8% CAGR over the past 9 years, way above management’s long-stated goal of MSD-HSD growth. Sales have only declined in 2014, a period when Fox began losing some of its spec position in the market. This is something we can appreciate in the following chart from VitalMTB (widely known mountain biking page, popular for its audience surveys), where Fox lost considerable mindshare beginning from 2013 until it recovered in 2016.

Fox’s management has stated in past earnings calls that they consider these surveys to be a relevant benchmark for their products, which tend to be highly influenced by the launch of successful products.

For example, in 2017, the launch of Fox’s Transfer seatpost launched it to the first sport in the survey, going from 7.5% to 22.1% in one year.

Going back to the company’s SSG revenue history, most of its success has come from:

Industry growth due to the introduction of E-Bikes into the mountain bike segment starting from about 2018. E-Bikes comprised about 35% of the European bike business and 15-25% of the American MTB business in 2019. Today, demand for these bikes is growing faster than pedal bikes, especially in Europe.

Increase of ASPs due to product innovations such as the introduction of Live Valve in 2018, which so far only touches the top 1% of Fox’s sales (2018 Data)

Expansion of the aftermarket business through new relationships such as the one established with Quality Bicycle Products in 2019 (Used to sell all of Fox’s bike brands before, except for Fox), which services more than 5,000 bicycle retailers.

Market share gains in recent years.

The recent boom in 2021 was mostly due to the pandemic-related trends we’ve already covered in previous sections, which led to bike shortages across the world (lead times were up north of 400-500 days at one point for some components).

It was well known that the levels of growth experienced during 2021 and 2022 were not sustainable and revenues in SSG have already begun correcting in H1 2023. 2023 Q1 SSG revenue was down 30% YoY and revenues for the full year are expected to be down 30%-35% as the industry is having to deal with the oversupply caused by outsized demand paired with supply chain disruptions.

Put simply, half-built bikes, for which Fox had already sold components, were stuck in the channel due to the lack of the remaining pieces needed to complete them. These bikes have just recently begun being finished and sent to dealers as the suppliers for the missing components caught up. This means that Fox will only be receiving OEM orders for its products after these bikes are sold-through to end customers.

This issue is mostly predominant with bigger OEMs, which have been forced to discount their existing models. These OEMs have also been reluctant to introduce ’24 models, as they would have to discount the ’23 bikes even further. It is important to note that these discounts do not affect Fox, as it has already received its respective compensation for the components it sold to the OEMs. In fact, the more aggressive the discounts, the better off Fox is going to be, as it will allow the company to resume receiving orders from these OEMs sooner.

To offset this issue to some degree, Fox has leveraged its relationships with smaller OEMs, which have responded better to ’24 products as they have less inventory in the system.

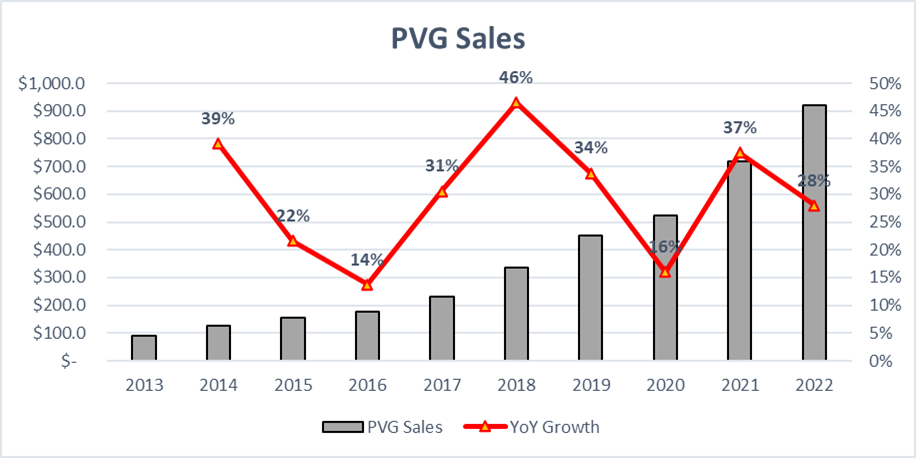

PVG

We can easily appreciate how the PVG business has grown at a much faster pace than SSG, growing at a 29.2% CAGR over the past 10 years. PVG growth tends to be non-linear, as it is subject to new vehicle introduction timing,

Most of this growth has come from Fox’s virtuous cycle we covered in the first part, where aftermarket adoption led to OEM wins and these OEM wins then led to further aftermarket adoption.

It is important to note that Fox was able to grow its PVG sales in the double-digit range during 2020 & 2021 even when its OEM automotive customers were forced to shut down their operations right when they were about to do a model year shift, which later caused various delays in vehicle releases.

What allowed Fox to offset these headwinds was the upfitting business, as revenues would’ve declined 1% in 2020 if we exclude the SCA acquisition. Strong sales in the aftermarket and great demand in the powersports segment were also a big help in offsetting the issues at the auto OEM level.

This trend is expected to reverse by 2024, as auto OEMs get back online, with powersports and upfitting now expected to slow down.

PVG OEM Wins

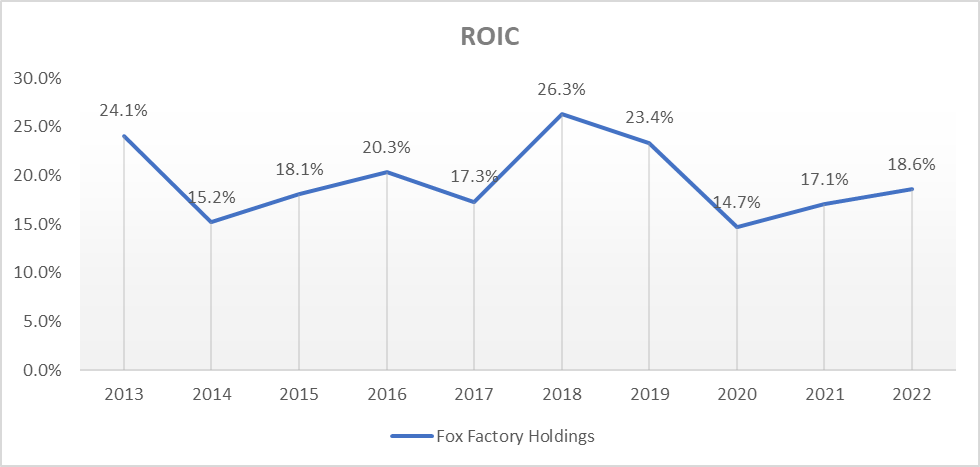

ROIC

Sadly, there aren’t any relevant competitors to compare Fox Factory’s ROIC to as we couldn’t find any standalone public suspension businesses. The only somewhat comparable company would’ve been Tenneco, which had a division where it sold its Öhlins and Rancho shocks, however, it recently went private.

Fox mostly complies with the newsletter’s 15%+ ROIC hurdle rate.

Expense Management

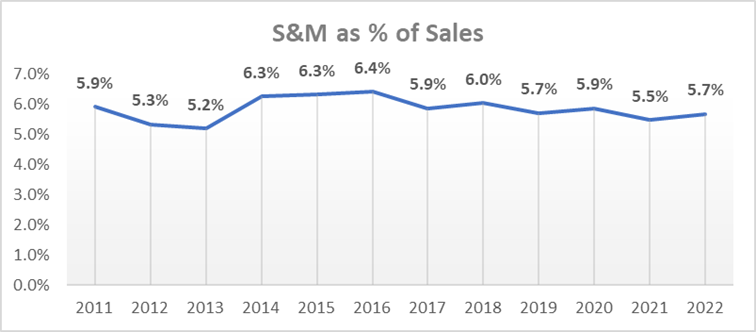

S&M

Selling and marketing expenses have mostly stayed flat over the past 10+ years. Management has stated many times that this is an area where they are not expecting to obtain operating leverage, and they’ll continue to invest in sales, marketing and R&D, as these are the engines of Fox’s growth.

With the strength of the Fox brand being one of the company’s biggest assets, marketing expenses are an essential component of its business model.

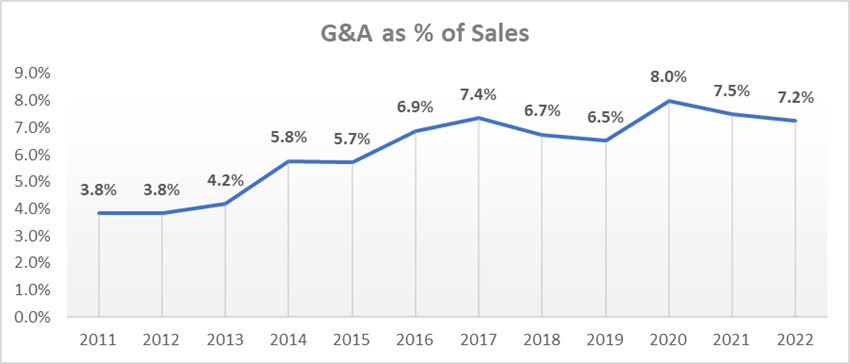

G&A

The management team had stated in the past, that as Fox began to obtain more of its revenue from larger OEMs, the company would be able to benefit from SG&A leverage. However, this has proven not to be true as G&A expenses have expanded by 340 bps as % of sales in the analyzed period above.

Most of these increases in costs have come from acquisition-related expenses, employee compensation and the growth of the upfitting business.

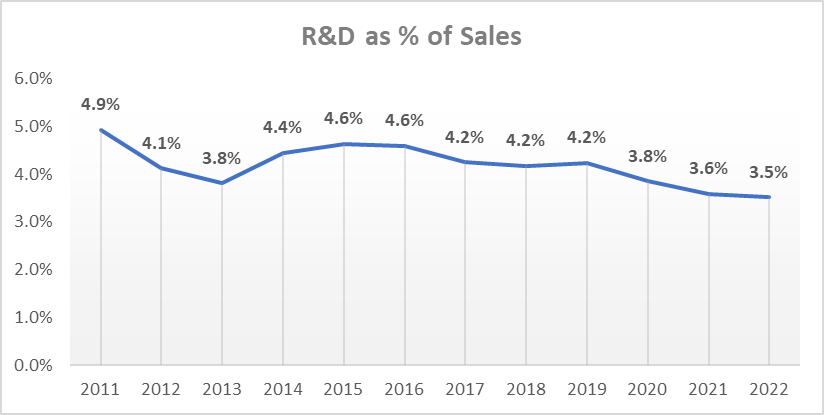

R&D

Product innovation is essential for the company to maintain the position of its products as top-performance components, making R&D expenses a non-negotiable for the business.

R&D expenses may lag revenue growth during periods of excessive growth, such as in the past 3 years. This is because there are only so many talented engineers that Fox:

Can find.

Can integrate into its operations while maintaining the caliber of talent it demands.

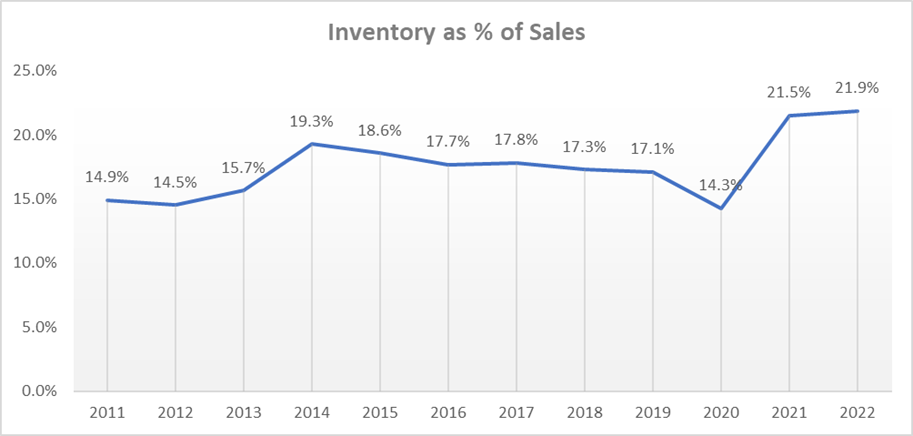

Working Capital

The company’s inventories have aggressively risen as a % of sales in the past 2 years. The main reason behind this is that, as many companies have done, Fox began building up on safety stock of raw materials to offset any possible issues at the supply chain level like the ones it experienced during 2020. Management plans on releasing these working capital investments once supply chain constraints begin easing.

Although a portion of this inventory buildup is voluntary, inventories also have risen due to Fox being unable to finish its products because of missing components:

“One of the things you’re seeing is our inventory, it still remains high. That’s a function of long lead times where you can get 90% of the components you need, but you can’t get the final 10% to complete the product. So those challenges in the supply chain, especially in the Powered Vehicle side, continue. And I think those will continue as I mentioned in my prepared remarks, for the balance of the year.”

—Mike Dennison, CEO (2022 Q2)

Another important aspect of Fox’s working capital are prepaid chassis for its upfitting business. These chassis have a mix dynamic to them, as the ones that Fox prepays come from Jeep and Ram. Therefore, the more Jeep and Ram models the company is upfitting compared to GM or other OE models, the higher the prepaid balance becomes.

Over the past few quarters, the company has worked on readjusting the past behavior it had to adopt during the pandemic, where it placed a prepayment on every chassis it could get its hands on, switching to a more optimized level as OEM production plans begin to stabilize.

Fox was able to take its chassis inventory from 12-15 months’ worth of chassis back in the pandemic to 6 months as of the most recent quarters, something they can still further optimize.

Capital Allocation

The management team has stated that Fox’s capital allocation priorities are:

Investments to support the growth of the business, such as expansion of production facilities.

Strategic acquisitions that meet Fox’s financial and strategic criteria.

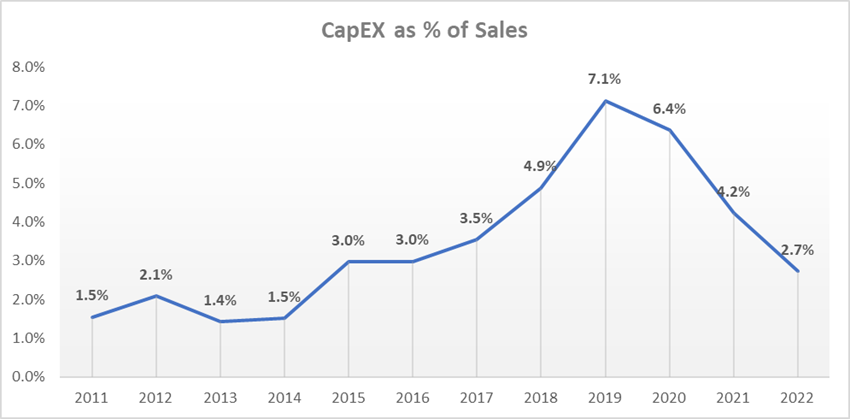

Capital Intensity

Fox’s long-term goal is for CapEx to stay in the 3%-4% of sales range. However, as can be seen above, this can vary from time to time depending on specific expansions made by the company.

The most relevant variance we can appreciate in the previous chart comes from the construction of the Georgia facility made during 2019 and 2020. CapEx considerably went down during 2022 and the CEO gave the following explanation:

“We’ve built a lot of infrastructure. We’ve spent a lot on CapEx. So this is just a good chance for us to pause and think about CapEx and think about headcount a little bit differently and make sure that we’re kind of lagging that growth. I think we’re really well positioned right now with the infrastructure we have and the capacity we have.”

—Mike Dennison, CEO

Management believes that the current capacity will be sufficient going up to its 2025 expected revenue. However, they are already looking at some additional lower-cost regions for manufacturing in the future, but that CapEx investment is not expected to happen in 2023.

Acquisitions

Since its IPO in 2013, Fox has been very active in the acquisition market, as you can see in the following timeline:

When looking for acquisition targets, management is seeking to find great companies selling a great product ran by a great team. This is a very similar approach to the one we have at Moonlight Capital, especially if we take into account the following quote:

“We like to get things at a value. So we like to buy assets that are not premium priced.”

—Mike Dennison, CEO

Acquiring businesses in adjacent markets allows Fox to leverage its global marketing, engineering, distribution and supply chain resources to easily improve the operations of the companies it acquires.

Fox does not actively look for these acquisitions or participate in auctions to buy these businesses. Most of the time, companies come up directly to Fox seeking to be acquired. This is something we will cover more in-depth as we dive through the company’s most relevant acquisitions.

Management has stated that they prefer to buy larger companies rather than smaller ones, as buying small companies takes about as much work as buying a big company while not really moving the needle for the company’s sales. However, if they find a technology or a business that gives them a capability they didn’t previously have (such as Ridetech or Shock Therapy), they’re fine with doing smaller acquisitions.

Below we’ll dive into Fox’s most relevant acquisitions over the past decade:

2014 - Sport Truck USA

Price paid: $44 million.

Revenue AToA: $34 million.

EBITDA multiple: 6.3x

Sport Truck used to be Fox’s largest aftermarket distributor. Through this acquisition, the company was able to enter into the lift kit solutions market and also get hold of Sport Truck’s distribution channel.

2014 - Race Face/Easton

Price paid: $30.2 million.

Revenue AToA: $23.6 million.

EBITDA multiple: 7x

Through this acquisition, Fox entered into various new bike markets, including wheels, pedals, handlebars, among other various components. It also allowed it to enter into the road bike segment, giving it the ability to gain some experience outside of mountain bikes and expand the universal things it could work on.

Race Face/Easton revenue is expected to grow in the HSD range over the long term. Fox later integrated the operations of Race Face into its Taichung facilities in 2018.

The most important aspect of this deal is that it turned Fox into a more complete supplier of bike parts, complementing its legacy suspension offerings. This allowed Fox to better compete with a company like SRAM (Owner of RockShox), which can offer OEMs with a full bike package.

2015 – Marzocchi

Price paid: $1.65 million

No revenue or multiple paid data is available for this acquisition as Fox didn’t acquire Marzocchi’s ongoing operations, buying some of the company’s mountain bike assets instead (names, IP, relationships, etc), which were related to forks and rear shocks. This left the motorcycle portion of Marzocchi’s operations out of the deal.

This acquisition showed up on Fox’s doors when Tenneco was desperately looking for a buyer as it failed to successfully integrate Marzocchi under its wing after buying it back in 2008. Marzocchi was not expected to survive in the state it was prior to being acquired by Fox.

“The challenges are such that all of the initiatives we've taken are insufficient to achieve viability in a highly competitive and slow-growth market. Despite the great efforts by the Marzocchi team to improve performance and reduce costs, our business model is not sustainable in this environment. We are actively seeking potential buyers for the business.”

—Andrea Pierantoni, Marzocchi Sales Director

According to our research, the Marzocchi brand was widely respected and had a very loyal customer base due to its products known for their sturdiness and ease of use. However, it began losing its strong position due to two important events:

2008: After being acquired, Tenneco unsuccessfully moved Marzocchi’s operations to Taiwan, where product quality took a nose dive. A former Marzocchi customer comments: “Marzocchi ruled until 2008 when they decided to go cheap and got bit in the ass hard.”

2012: Sr Suntour used to assemble Marzocchi’s forks and shock in Taiwan. However, after talks ended between Suntour and Marzocchi for a possible acquisition (from ST), Suntour stopped assembling Marzocchi’s products. Marzocchi lost two model years as a result before finding a new assembly partner, further worsening the state of the company’s operations and the image of its brand.

Marzocchi was experiencing other various difficulties, among which one of the most relevant were ever-present labor issues in Italia.

Due to its critical state, Fox was able to buy Marzocchi at a bargain price, recording a $315 million gain (net of tax) to reflect the excess of the fair value acquired over the consideration paid.

“Marzocchi … wasn’t exactly a transformational acquisition. We kind of bought it, I hate to say off the bargain bin, but that’s probably not far from correct.”

—Larry Enterline, Former CEO

Marzocchi’s expected sales for 2016 were $2 million, operating at basically breakeven profits ($0.01 per share operating loss). The business then became accretive to Fox’s results in 2017 as its operations were moved from Italy to Taiwan.

This deal helped the company further expand the penetration of its bike suspension products across lower price points (Below the recently launched Rhythm series at the time) without having to dilute the Fox brand.

Fox was then able to leverage its aftermarket distribution and OEM relationships to easily drive top-line growth for Marzocchi.

After various investments in the Marzocchi brand such as the sponsorship of the 2019 proving grounds, the widely recognized Bomber Forks began winning awards as value products of the year in 2019. Making Fox’s endeavor of positioning Marzocchi as a value alternative to its legacy shocks successful 4 years after the acquisition.

2017 - Tuscany Motors

Price paid: $66.75 million.

Revenue AToA: $40.8 million.

EBITDA multiple: 9x

The Tuscany acquisition marked Fox’s first entry into the upfitting business. Fox initially bought 80% of the company and later bought the remaining 20% stake in 2020.

Tuscany was also a customer of Sport Truck and Fox’s shocks prior to the acquisition. Fox’s main goal with the deal was to further develop the off-road capable on-road vehicle segment where its legacy products became very predominant since the launch of the Ford Raptor.

Tuscany is expected to grow in the double-digit range over the long term.

2019 – RideTech

Price paid: $14 million.

Ridetech is a manufacturer of traditional, coil over, and air suspension systems for muscle cars, trucks, and hot rods. As per usual, Ridetech was a Fox customer prior to the acquisition.

Sadly, we couldn’t find any available data for revenue or EBITDA figures at the time of the acquisition. However, Fox expected sales contribution from Ridetech for its first year after being acquired to be in the range of $6-$8 million after the elimination of inter-company sales.

Just like Sport Truck, Ridetech was an aftermarket play for Fox, and in order to align the interests of the Ridetech management team, Fox left 20% of the shares to them.

2020 - SCA Performance

Price paid: $331.8 million.

SCA has been Fox’s biggest acquisition so far. Similar to Tuscany, SCA is a vehicle upfitter focused on full-size trucks under brands such as Black Widow, Rocky Ridge and Rocky Mountain.

This acquisition was complementary to the Tuscany business, expanding Fox’s North American footprint for manufacturing, which provides incremental efficiencies and capacity utilization. Due to various other synergies, the company then decided to essentially combine SCA and Tuscany into a single business, making sure to maintain the segmentation between the offerings of both units.

Fox didn’t give annualized data for SCA’s revenue and EBITDA, however, with some information given by management, we estimate that SCA generated about $107 million in revenue in 2020 and about $30 million in EBITDA, translating into an acquisition multiple of 11x.

2021 - Sola Sport

Price paid: $486,000.

Sola Sport was both a small and simple acquisition for Fox. Sola was a distributor for all of Fox’s brands in Australia. The main objective behind this acquisition was to give Fox an initial foothold in Australia (both for PVG and SSG) as it begins to expand internationally.

2021 - Outside Van

Price paid: $15.2 million.

Outside Van is a premium upfitter of adventure vans on the Mercedes Sprinter platform. At the time of the acquisition, the company was doing about a couple hundred units of custom vehicles every year. In Fox’s most recent earnings call (2023 Q2) the CFO mentioned that they see Outside Van easily doubling this level of units in the near future. This statement seems very plausible if we take into account that back in 2021, Outside Van was struggling to keep up with the demand for its products, having 2 years’ worth of backlog in its books.

Fox’s management saw this acquisition as an opportunity because the adventure van customer demographic has a considerable overlap with mountain bike enthusiasts, giving the company a marketing opportunity with its existing customers.

2021 - Shock Therapy LLC

Price paid: $36.8 million.

Shock Therapy is a premier suspension tuning company in the off-road industry headquartered in Arizona. The main objective behind this acquisition was to help Fox increase its services business by creating a meaningful and personalized ecosystem around its enthusiasts and end consumers. ST was doing about $20 million a year in revenues and was growing slightly above Fox’s PVG business at the time of the deal.

“It's not large. It's really the technology and some of the thinking that we're getting from Shock Therapy that we can use in the rest of our business that is so meaningful. And from a margin perspective, it's not dilutive.”

—Mike Dennison, CEO

2023 - Custom Wheel House

Price paid: $131.6 million.

Custom Wheel House offers high-performance tires and wheels for powered vehicles. This acquisition provided Fox with significant vertical integration and synergistic opportunities, especially for its lift kits, upfitting businesses and even for the recently acquired Shock Therapy segment.

“This acquisition will enable us to continue to create an ecosystem of high-performance integrated products for our enthusiast customer base. Our ability to weave together these iconic brands to build a robust platform of products is unique amongst our competition.”

—Mike Dennison, CEO

Fox quickly decided to invest into additional distribution centers and CWH’s capacity in order to provide those wheels through its outside van and upfitted truck businesses.

The CWH segment is expected to contribute about $60-$70 million in revenues during 2023 while being accretive to Fox’s margins.

Summary

That was our best attempt to summarize Fox’s most relevant acquisitions. As you can see, most of them have happened in the PVG group of the business. The reason behind this is that, with the explosion of bike sales during recent years, valuations for possible acquisitions in the SSG segment have skyrocketed, and Fox has been reluctant to acquire these businesses at these high prices, which have only begun to come down to more reasonable levels during the most recent quarters.

This trend also happened in PVG, but to a lesser degree, allowing Fox to pick up some good deals here and there, with multiples especially coming back to attractive levels since the back half of 2022.

Return to Shareholders

Dividends

The company hasn’t paid a dividend since its IPO, and the management team hasn’t shown any signs that they intend to pay one in the near future.

Buybacks

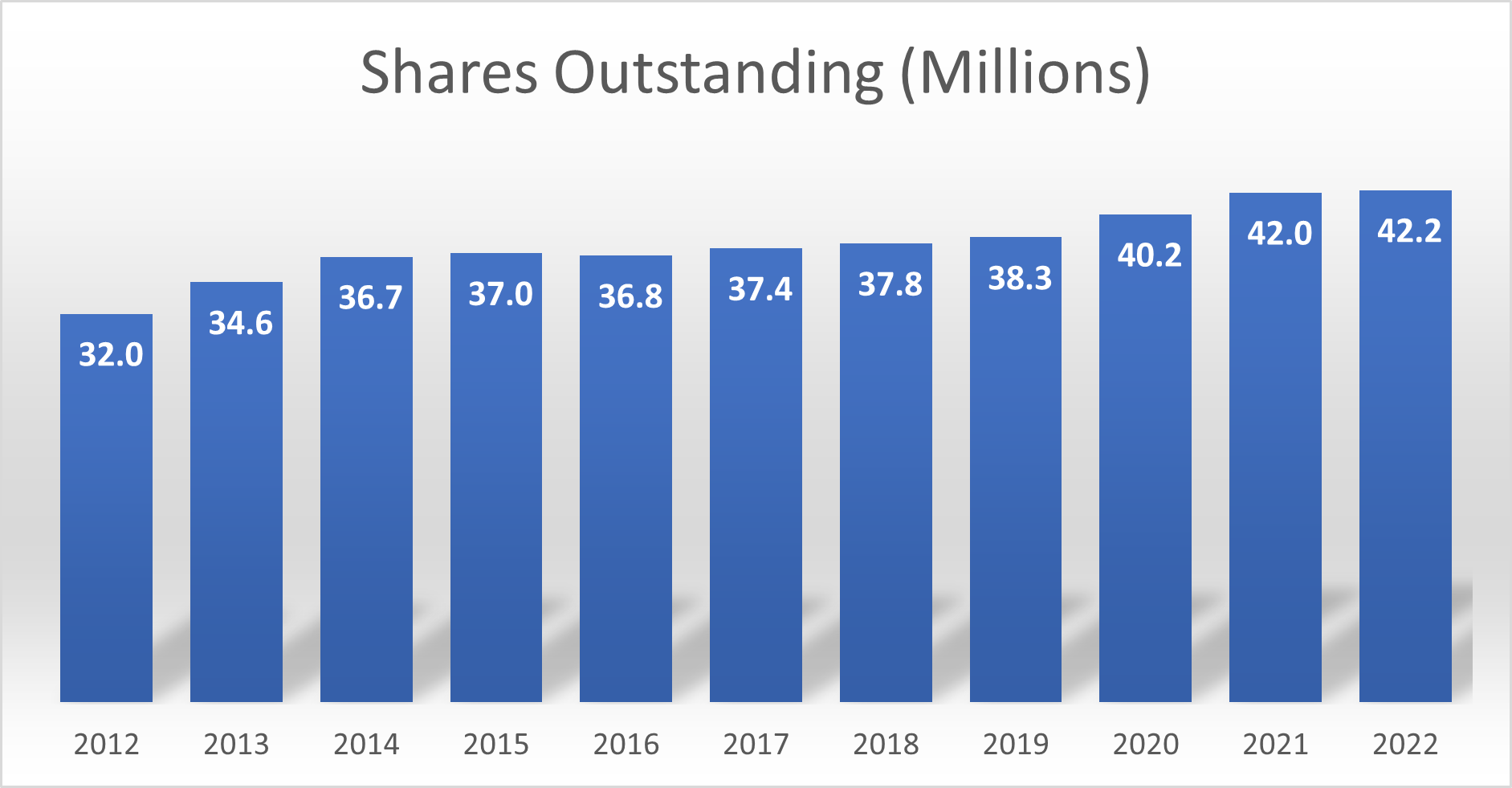

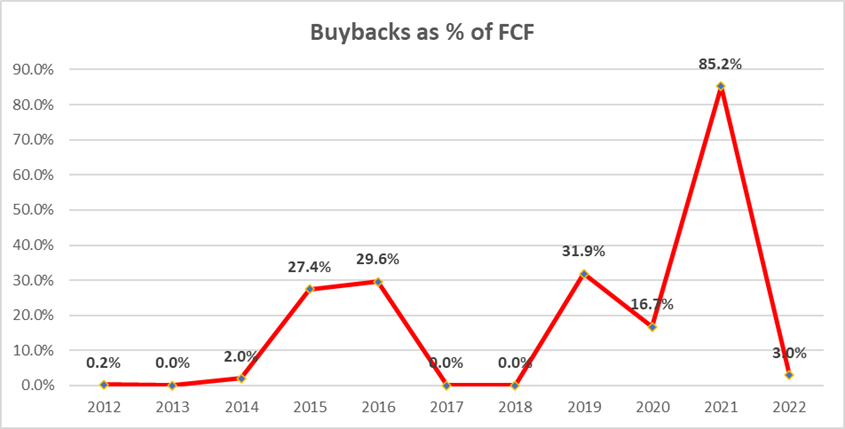

Similar to the trend seen in dividend payments, Fox is not very active when it comes to share buybacks either, being a net issuer of shares in the past 10+ years. (2.8% CAGR).

Except for 2021, where FCF was depressed, buybacks have never represented a significant part of the company’s FCF investments either.

Growth Plan

It took the company four decades to achieve its first $1 billion in revenue, and now the management team expects to reach $2 billion in revenue four years later, by 2025. This does not take into account any possible acquisitions Fox could make along the way.

For the next few years, due to the outsized growth the company has recently experienced, the PVG segment is now expected to deliver lower levels of growth, while SSG is expected to experience a sizeable decline before returning to its long-term growth rates.

Over the long term, however, PVG is expected to grow in the double-digit range and SSG in the MSD-HSD range, both organically. This combines into a long-term growth rate for Fox overall in the HSDs.

Note: The growth rate expected for PVG already considers OEM wins over time, so these are not incremental.

The three pillars of Fox’s growth are expected to be:

Market share.

Market growth.

Market making.

Below we’ll dive into the main factors expected to drive Fox’s growth over the coming years:

International Expansion

As we’ve already mentioned, Fox’s sales are negligible outside of NA and Europe, leaving a huge opportunity for the business to expand internationally.

The first countries Fox had put its eyes on were Australia and Germany, already having set foot in the former through the Sola Sport acquisition and on the latter through the acquisition of Toxoholics and the opening of a new facility in 2020.

Other current low-hanging fruits management sees in terms of international expansion are China and the Middle East. This is not overly built into the 2025 target, therefore it is intended more as a long-term strategy.

Focusing on the SSG segment for a second, we see Fox taking advantage of its more accessible Marzocchi brand to initially penetrate into emerging markets such as South America, where Fox-branded components might find it more complicated to pick up in terms of volumes due to their higher price tag.

Increase of ASPs due to innovation

Although Fox’s products may historically look very similar from the outside, most of the magic happens on the inside. The company’s continuous investments in R&D eventually develop into product innovations that drive average selling prices higher, something both CEOs have already mentioned is a core function of Fox’s strategy:

“We like to use innovation and get price per function. So we like to get price when we’re bringing more value through performance and features of the product. And I think we have the capability to do more of that. I think that’s been a consistent driver. I don’t know that there is a place where as innovation continues that you run up against any absolutes here in price.”

—Larry Enterline, Former CEO

“We do try to drive innovation and technologies and things like that to drive price increases. And as we know, and can envision, over the years the price points of our products have consistently gone up year-on-year. So we’ll focus on that, and we'll continue to use innovation and technology to drive value, which drives product price.”

—Mike Dennison, CEO

The most notable product innovations we can mention are Internal Bypass and Live Valve, with the latter being remarkably important for the future of Fox, especially for the PVG segment. Although we won’t dive much into detail here, in summary what Live Valve (technology developed in conjunction with Polaris) does is, through various sensors, gather information about the terrain and the vehicle’s current state (whether it is pointed up, down or in the middle of a free fall, for example). That information is then sent to Live Valve’s microprocessor to adjust the suspension accordingly in a matter of a few milliseconds.

For example, if the sensors identify that the vehicle is in the air, it will automatically stiffen the suspension in order to better absorb the jump.

“The bottom line is that Live Valve represents the most useful and important suspension innovation to emerge in a decade of boring improvements. It works great and I don't want to ride without it.”

—Comment from Pinkbike Magazine

The importance of Live Valve lies in the fact that it is expected to become a core technology for the future of Fox’s developments in the suspension industry. As vehicles continue to become smart and connected, it will become a key component of these platforms and grow to become a bigger part of Fox’s sales.

This is also one of the main reasons Fox seeks to become vertically integrated in the bike segment, where the company is expected to benefit from adding products into its portfolio as bikes begin getting to the point where all the components start talking to each other. The CEO gave the following example for the future of connected products:

“The suspension of a bike will be connected to your phone and your suspension can automatically get adjusted depending on the weather or your specific location. It may also give you suggestions depending on settings previously used by riders that were there. This is expected to absolutely happen by 2025.”

—Mike Dennison, CEO

Suspensions will continue to become more complex as these electronic components get packaged in the legacy mechanical structure that has been perfected over many decades, leading to higher ASPs and further differentiation for companies like Fox.

“I can’t imagine it NOT being part of the mountain bike future [Electronically-controlled suspensions]. The smarter the suspension, the better job it can do - at least in theory. The main downsides are cost, complexity and resistance to change - 'tradition.' I think those barriers will diminish as time goes on

—Bob Fox, Company Founder

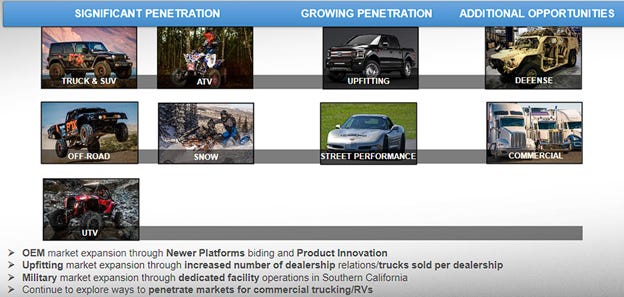

Growing Penetration and Entrance into new existing markets

Expanding into relevant adjacent markets and growing penetration into already covered markets is another key component of Fox’s growth strategy.

“Although we were originally 'forced' to diversify into other markets besides motocross, we are now actively on the lookout for new markets where our racing heritage may offer an advantage. We find that involvement in many different markets broadens and strengthens us technically. We sometimes learn something new in one market that has applications in a different market. We call this 'cross-pollination' - which we consider a major advantage of working in diverse high-performance markets”

—Bob Fox

Off-Road Powered Vehicles

The powersports industry is a perfect example of how Fox has begun to further penetrate its existing markets. First through the acquisition of Shock Therapy, and later through the acquisition of Custom Wheel House.

Fox can also further increase its revenue per vehicle with existing OEM customers by:

Increasing the number of components it includes in the platform.

Upgrading the technology used, going from an IBP component to implementing Live Valve for example, like they did with the Raptor.

Military

Fox used to have defense contracts back in 2015, however, not many comments have been made in that regard since then. With military applications still being mentioned in Fox’s 2022 10-K, we can infer that Fox continues to participate in this market but revenues might not be considerable.

The most recent comment we could find regarding this topic was on Fox’s 2021 Investor presentation, where the CEO mentioned that they really liked this business and were looking to further expand Fox’s penetration into this segment, as it is probably one of the company’s highest margin products in PVG and contracts are usually long.

CMVs

The commercial motor vehicle market is one Fox has been looking to expand into without much success so far. This expansion is both an OEM and aftermarket play, with Fox approaching the AM first in order to gain the public’s confidence to then drive OEM deals.

Fox first began testing shocks and collecting data on 15 vehicles back in 2017 and then launched its first products for long-haul (18 wheels) semi-tractors in 2018. This launch was mostly made through Raney’s Truck Parts, which is one of the largest online retailers catering to the independent owner/operator accessory aftermarket.

Fox’s strategy is to offer a spend-to-save proposition, where the main benefits CMV drivers can obtain from Fox’s products are related to comfort and safety, also saving money on aspects such as:

Maintenance intervals.

Fuel costs.

Tires.

Although the application may be quite different, the company was still able to leverage some of the technology it had developed and fine-tuned in off-road applications.

Today, Fox has continued to grow in the aftermarket of this segment, mostly fulfilling demand at the owner-operator level, however, management believes they have a lot of growth to achieve before they get to the point of winning their first OEM deal.

Bikes

Fox’s main opportunity in the bike market is to further gain market share in its underpenetrated categories (cranks, wheels, handlebars, seatposts, etc), where its position is not as strong as in suspensions. The company plans on doing this through the introduction of innovative products and scaling its production capabilities.

Bike wheels is an area where Fox has significant demand, and that’s why their focus there is to scale production. The main challenge with wheels is that they’re bulky and expensive to ship.

The launch of products specifically made for E-Bikes has also helped Fox further strengthen its position in the bike industry, with options such as:

E-Tuned, which are legacy mountain bike suspensions tuned specifically for the needs of e-bikes.

E-Optimized, which takes it a step further with a beefed-up chassis.

E-Live Valve, which incorporates live valve technology into the E-Optimized offering.

AWL (Adventure Without Limits) forks specifically for e-SUVs.

Management estimates these new markets (E-MTB, E-SUV and Gravel) offer Fox a $1.1 billion market potential for 2025.

Another important aspect of Fox’s growth will be the broadening of the price points it covers in the industry. For example, setting Marzocchi aside, Fox currently plays in the $2500-$15,000 USD bike price point, where there are about 1 million of those bikes produced every year. However, if we take into account the price point where Marzocchi plays, which is the $1,000-$2,500 range, that’s another 1 million bikes added to Fox’s TAM.

The $1k-2.5k bike price point is also a very attractive high-margin business with great growth ahead that could possibly add a lot of volume.

Market Creation

Fox intends to grow not only through the growth of existing markets or by taking market share, but also by making new markets like they did with Raptor in 2010. At the time, Ford came to Fox thinking about doing something different, which led to the creation of a Baja race-ready truck that could be used as a daily driver.

Once the first model came out of the factory, there was nothing competing with the Gen 1 Raptor. The market only began to catch on by the launch of the Gen 2 where alternatives like the TRX from RAM were released.

“The Ford Raptor has kind of launched an entire new sector of trucks. And obviously that benefits us and it creates conversations that we probably wouldn't have had before with different folks.”

—Mike Dennison, CEO

Another example of market-making happened with the release of the first side-by-side back in 2008, when Polaris decided to take the traditional UTV that looked like a bulked-up golf cart and turn it into a more badass vehicle. At that time, Fox had 4 SKUs with Polaris, having over 100 SKUs today.

Management anticipates that over the next 5 years, at least one new market or two will be created.

Adding new dealers to the upfitting business

Diving specifically into the upfitting business, Fox plans on continuing to add new dealers to SCA and Tuscany’s customer base. Today, Fox has relationships with about 2,200 dealers for its upfitting business, and management estimates that there are about 15,000 dealers just in North America.

The industry has experienced a shift in consumer behavior after COVID, making people more willing to buy trucks online from dealers that are not close to their locations. Buying a truck from a different state, for example.

How Fox leverages this is, for example, if someone buys a truck from a dealer in Florida while living in Arizona (because it wasn’t available in a dealer close to him), Fox will go up to that Arizona dealer that isn’t a Fox dealer yet and tell them ‘You just missed a $100,000 truck sale, because you’re not carrying our trucks.”

Fox currently has about 4.7 trucks per dealer, and with how fast these are selling, the CEO believes that number should be at least 7.

The company was recently unable to focus on growing its dealer count as it couldn’t keep up with the demand for its vehicles due to supply chain disruptions. However, with the supply chain being somewhat back to normal, the company is now pushing to build relationships with new dealers. The current goal is to expand from 2,200 dealers to 2,500 dealers and beyond in the upfitting business over the coming year.

Management

Fox previously had a long-standing management team that had held their positions since the IPO of the company. Larry Enterline served as Fox’s CEO from 2011 to 2019 and Zvi Glasman served as Fox’s CFO from 2008 to 2020. As can be easily seen through Fox’s number, they did a stellar job at the helm of the company, turning a shock-selling business into a $2.5+ billion monster.

Larry was eventually replaced by Mike Dennison in 2019 Q2. Mike was previously a member of Fox’s board, later the PVG president and Larry convinced him to become part of the management team.

Zvi Glasman announced he would be stepping down as Fox’s CFO right after Larry left his position as CEO. Fox then went on to experience very high turnover in the CFO position, with Scott Humphrey joining in 2020 Q3 and later leaving in 2023 Q1 and Dennis Schemm joining the company one quarter later. These are two personal concerns I’ll be commenting on more deeply in my conclusions of the write-up.

Thomas Fletcher is the current PVG president, coming from Flex just like the current CEO. Chris Tutton is the current SSG president, and he served as the president of Race Face/Easton from 2014 to 2018 until the company was acquired by Fox.

Integrity, Intelligence & Ability to Deliver

Below are some quotes/comments from Fox’s executives that exhibit the types of behavior we look for in a management team:

Long-term thinking ✅

“I think we like to focus on the longer-term targets and optimize this company’s efficiency not on a quarter-to-quarter basis, but more on a sustainable long-term basis.”

—Larry Enterline, Former CEO

During 2020, the company decided not to take advantage of the outsized demand for its product to make aggressive price increases: “We’ve got really long-term partnerships with some really great customers. And to go in in a market like this and try to increase your prices, just because they're really dying for products and volume for life is not really a good long-term strategy for a partnership … We try to avoid scenarios like that.”

—Mike Dennison, CEO

Intelligent M&A ✅

“As we have said, since we’ve gone public, we’re not going to do a deal just for tonnage, right? We’d like to get an acquisition that would meet our strategic and financial requirements. It is a frothy market out there, and we’re going to continue to be disciplined. So if there’s a good deal to be had, a willing dance partner at the right financial price that has a good fit for Fox, we would be interested.”

—Zvi Glasman, Former CFO

“We've used different mechanisms in each deal to ensure that management was aligned with Fox. In the case of Sports Truck and Race Face, we did earn-out. In the case of Tuscany, we bought 80%, not 100% of the company. In the case of Ridetech, they took a fair bit of the purchase price in stock. We use different mechanisms for different situations. We think they all depend on the particulars of the situation and we think this aligns the interest of management with us.”

—Zvi Glasman, Former CFO

“And the good news is, if there is good news, in a bad recession or a bad economy, things get cheaper. And that’s a good thing for us, using our dry powder to pick up things that we think are long-term valuable to the company.”

—Mike Dennison, CEO

Ignoring Noise and Focusing on What Matters ✅

“We're going to keep our teams focused on developing performance-defining products that passionate customer base that we have wants. We got all kinds of macro and noise going on with the tariffs, potential downturns, interest rates going up. We're going to worry about what we can control. We're going to be cognizant of the environment. And we're going to keep trying to satisfy those customers. I think if we do that, we're going to be just fine.”

—Larry Enterline, Former CEO

Intelligent Management of Capital ✅

“When we did the equity raise, it was a function of the markets becoming available for us to take that kind of action and really put us back on to an offensive position. So really, when we think about equity, we think about having the ability to turn from defense and kind of in the middle of the pandemic change to offense as we come out of it to look at companies that are a good fit for us from an acquisition perspective and fit the criteria of the business we run. So first and foremost, having a strong balance sheet gives us that ability for offense, but it does allow us to have a strong liquidity position should this pandemic continue on into 2021 and beyond. it's a little bit of offense and a little bit of defense.”

—Mike Dennison, CEO

“We’re steadfastly committed to a stronger customer-focused business that generates sustainable profitable growth with returns well above the cost of capital.”

—Mike Dennison, CEO

Ability to Deliver ✅

By reading all of the available material we could find in terms of past Fox’s presentations, we’ve seen management has consistently delivered on their past guidance/plans, whether that relates to margin improvements or sales growth. In fact, they tend to overdeliver.

Compensation

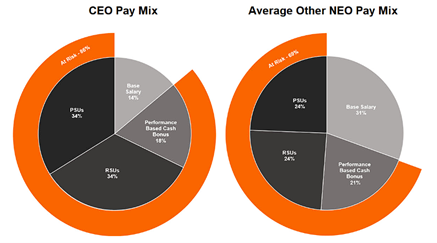

Like most great businesses, Fox employs a pay-for-performance compensation philosophy, with 86% and 70% of the pay mix coming from at-risk compensation for the CEO and other NEOs, respectively.

We’ll dive into each component of this compensation plan:

Performance-based cash bonuses: The CEO and CFO receive bonus yearly payments depending on the achievement of company-set target adjusted EBITDA, while other executives receive bonuses depending on both adjusted EBITDA and other individual performance objectives (75% and 25% weighting respectively). While adjusted EBITDA is not something we consider an ideal metric and would much rather prefer to see a metric like FCF in this regard, it’ll have to do.

RSUs: RSUs offered to NEOs vest over 3 years (33% each year). We would prefer to see a slightly longer vesting period for these.

PSUs: PSUs were recently approved in 2022. These vest on the achievement of performance goals related to ROIC and FCF, which we consider excellent metrics for a company to incentivize its managers to optimize.

Although Total Stockholder Return is not used as a performance metric, it is taken into consideration by the compensation committee when compensating NEOs.

Skin in the Game

Both executives and directors are mandated to acquire and hold ownership of Fox’s common stock having value equivalent to:

5x base salary for CEO.

3x base salary for every other NEO.

5x annual cash retainer for directors.

Both parties are given 5 years after the day of their employment to comply with these requirements. Breaking down the current ownership of the four most relevant executives as of the latest proxy we find:

CEO: Owns 3.35x his base salary.

CFO: Owns 0.9x his base salary.

SSG President: Owns 1.2x his base salary.

PVG President: Owns 0.4x his base salary.

Perhaps we’ve become very demanding after analyzing BRP, where the CEO held 107x his base salary of $1.2 million in the company’s stock, but we find these ownership numbers to be very low.

Financial Strength

Not many comments can be made regarding Fox’s balance sheet as it is remarkably conservative.

Fox complies with our <4 LT Debt / FCF ratio, and with considerable principal payments coming in 4+ years, we don’t see any issues in this regard.

“We are certainly pleased with our robust balance sheet, and I believe it to be one of the top defenses against any bumps in the economic environment that we may experience.”

—Mike Dennison, CEO

Competitors and Competitive Advantage

Competitors

SSG

Within the market for bike suspension components, Fox competes with several companies that manufacture front and rear suspension products, including:

RockShox (a subsidiary of SRAM Corp.).

Manitou (a subsidiary of HB Performance Systems).

SR Suntour.

DT Swiss

Cane Creek Cycling.

DVO Suspension.

Bos-Mountain Bike Suspensions.

Öhlins Racing AB.

In the market for other bike components, Fox competes with

SRAM.

DT Swiss.

Mavic.

Shimano.

The only public company between these is Shimano.

PVG

In the PVG segment, Fox competes with other companies that produce products for sale to OEMs, dealers and distributors, as well as with OEMs that produce their own line of products for their own use.

Within the market for off-road and specialty vehicle suspension components, Fox competes with:

ThyssenKrupp Bilstein Suspension GmbH.

King Shock Technology.

Icon Vehicle Dynamics.

Sway-A-Way.

Pro Comp USA Suspension.

Rancho ("Tenneco").

In the market for suspension systems, or lift kits, Fox competes with:

TransAmerican Wholesale

Rough Country.

TeraFlex.

Falcon.

ReadyLIFT.

Tuff Country.

Rusty’s Off-Road.

In the market for upfitted vehicles, Fox competes with:

Roush Performance.

DSI Custom Vehicles.

In the ATV and side-by-side markets, outside of vertically-integrated OEMs, Fox competes with:

ZF Sachs.

Walker Evans Racing (Recently acquired by Polaris)

for OEM business and

Elka Suspension Inc.

Öhlins Racing AB.

Works Performance Products.

Penske Racing Shocks.

for aftermarket business.

The only public competitor in PVG is Bilstein, which comprises a small part of the sales of the ThyssenKrupp conglomerate ($0.96 billion Euros or 2% of sales)

Competitive Advantages

Premium Recognized Brand with Strong Consumer Loyalty

Fox, due to its history in the industry with various successful product launches, dealer relationships, race wins and favorable media reviews and awards has developed a reputation for high-quality performance-defining products, allowing the company to sell its products at premium prices.

The company takes great effort to maintain its brands in the eyes of consumers. For instance, its Fox logo is prominently displayed on its Fox-branded products used on bikes and powered vehicles sold by its OEM customers, which helps further reinforce its brand image. Fox’s brand is mostly dominant in the SSG segment, where Fox and RockShox hold an effective duopoly in the bike suspension market.

“If you buy a phone, it's going to be Apple or Android. If you board a plane, it's probably built by Airbus or Boeing. If you're after suspension for your mountain bike, it'll most likely be from Fox or RockShox. The duopoly has been battling it out for MTB suspension supremacy for years, and while there are plenty of other brands out there, they corner most of the market because they make consistently good products.”

—Pinkbike Magazine

Fox’s strong position also allows it to gain bargaining power over its customers, which tend to willingly pick up price increases, as mentioned below:

“If you’re a seatpost manufacturer trying to sell to an OEM, the OEM has a lot of bargaining power, as a seatpost brand is more or less irrelevant to the consumer. However, if Fox comes up to an OEM intending to spec its forks, the OEM has much less bargaining power as a fork is a much more relevant part of a bicycle and the OEM might be able to sell more bikes if it includes a Fox fork on them due to Fox’s strong brand.”

—Comment from the Finanzas e Inversion Podcast

Bike enthusiasts tend to love the Fox brand, to the point that it is not uncommon to see them carrying the logo tattooed on their body.

Below are some quotes we consider build up on the strength of Fox’s brand:

“We are not a supplier, we are a product innovation company. And the difference between a supplier and a product innovation company is that our brand matters. We don’t make a shock that doesn’t have our brand on it, and they don’t usually build a truck where they don’t talk about our brand on that truck.”

—Mike Dennison, CEO

Track Record of Innovation paired with its Racing Culture

Being born in a racing environment, Fox has always pushed to make the best product possible. Mainly because in the top level of competitions, every second counts. This led innovation, including new product development, to become a key component of Fox’s growth strategy and its culture.

Another advantage of being involved in the racing scene is that Fox is able to get direct feedback from world-class professional athletes, which provide the company with unique real-time insights to improve product performance. This is done through their Racing Applications Development (RAD) program, which is used as a tool to develop products that are not quite ready to be released to the public. By testing the products in racing environments such as the toughest deserts, Fox can make sure that a) They can actually survive and b) They provide the rider a performance advantage.

“One of the benefits to being a part of motorsports and the rad system is we can make changes quickly. We jump at it, we build it, we test it before we ever release it to the market, which gives us a lot of freedom.”

—Fox Employee

Not only is Fox surrounded by professional athletes, but the Fox team itself is also very involved in the racing scene. Many of the members of the organization have a racing background themselves, further motivating them to make the best product possible.

“The racers push our products as hard as they practically can be pushed, to enable us to figure out what we need to do next to enable them to be even faster and better than they are today.”

—Tom Fletcher, PVG President

In summary, all of the suspension products that Fox eventually releases to the Aftermarket and OEM channels are born in racing.

“Racing becomes the proving ground for all of our new technology, because it’s so brutal. You can’t simulate that on a dyno or a wind tunnel or anywhere else in the world except for in the desert.”

—Fox Employee

Due to its diversification across various end markets, Fox can leverage successful product releases across most if not all of its product lines. For example, its initial success in the high-end ATV category led to the widespread adoption of Fox’s suspension technology in the side-by-side market.

The key to Fox’s success is to continue to innovate and stay in premium high-performance vehicles. If it continues to do that, no matter who wins, Fox wins. What we mean by this is represented by the following example: If you look at the top-end side-by-side offerings from the biggest OEMs (Honda, Yamaha, Kawasaki, BRP and Polaris), all of them have Fox shocks underneath their chassis. This means that, as long as Fox continues to stay at the top level of performance, whether Polaris gains share over BRP, or Honda suddenly dominates the market is all irrelevant for Fox, as it benefits from every single player.

Strong established relationships with OEMs

Another strong barrier of entry Fox benefits from is the relationships it has built with OEMs and distributors over decades in SSG and many years in PVG. This allows the company to, for example, buy brands like Marzocchi, and immediately stick their products into OEM frames.

Also, as suspensions continue to become more complex due to the introduction of electronic components, especially in PVG, Fox has to work more closely with its customers to build and implement suspension solutions. This makes it even more complicated for other companies to steal Fox’s customers.

Risks

The impact of the risks associated with international geopolitical conflicts. In recent years, diplomatic and trade relationships between the U.S. government and China have become increasingly frayed and the threat of a takeover of Taiwan by China has increased. Since Fox’s bike suspension manufacturing occurs in Taiwan, its business, operations and supply chain could be impacted by political, economic or other actions from China, or changes in China-Taiwan relations that impact Taiwan and its economy.

Dependency on a limited number of suppliers for some materials and components: Fox depends solely on Miyaki Corporation for the production of the Kashima Coating used on its bike suspension products. Although the company could obtain other coatings with comparable utility from other sources, the need to replace the Kashima coating could temporarily disrupt Fox’s business. Regarding the importance of this coating, which is used on the Factory fork line (most expensive one), Fox engineers claim that it cuts friction by 10%-12% compared to black anodized coating while also increasing hardness, which in turn increases scratch resistance and overall stanchion durability.

OEM customers seeking to vertically integrate such as Polaris with the Walker Evans Acquisition: Something important to keep in mind is that some of Fox’s competitors are also its customers. Due to Fox’s product development, the company has basically become a road toll for companies that seek to operate at the top level of off-road performance. However, Fox’s products tend to be quite costly, which explains why they are often limited to the top-end offerings of its customers. Fox could see a big hit to its sales if these OEMs decide to vertically integrate in order to get Fox out of the equation and cut costs. For example, Polaris has already acquired Walker Evans (suspension manufacturer), but whether their plan is to limit Walker Evan shocks to lower-end products or heavily invest in R&D to implement WE shocks in all of their products is yet to be seen.

Work stoppages or other disruptions at seaports could adversely affect Fox’s operating results. A portion of the company’s goods move through ports on the Western Coast of the U.S. Fox has a global supply chain and it imports products from its third-party vendors as well as its Taiwan facility into the U.S. largely through ports on the West Coast. The company has no control over the activities of dock employees or seaports and it could suffer supply chain disruptions due to any disputes, capacity shortages, slowdowns or shutdowns that may occur. This has previously occurred in 2014 Q4, when a port labor strike lasted longer than the company forecasted and ended up costing it $1 million or 150 bps in margins. Any similar labor dispute in the future could potentially hurt Fox’s results.

The professional athletes and race teams who use Fox’s products are an important aspect of the image of its brand. The loss of the support of professional athletes for its products or the inability to attract new professional athletes may harm Fox’s business. Sponsorship agreements typically restrict athletes and teams from promoting competitors’ products, however, Fox doesn’t usually have long-term contracts with these athletes. To the extent that a) These athletes decide to leave the Fox brand or b) They fail to have success in races and therefore lose popularity, the value of the Fox brand and therefore its sales could decline.

OEM business can be very volatile: Production disruptions from OEMs, such as the ones experienced during 2020, can adversely impact Fox’s results. Not only that, but the contracts Fox usually has with these customers are usually not long-term ones, meaning a vehicle can stop being produced any year, just like the Ford Raptor did in the past. Although Fox has managed to diversify its customer base since the production stoppage of the Ford Raptor back in 2014, the loss of relevant customers could cause a considerable decline in the company’s sales.

A relatively small number of customers account for a substantial portion of Fox’s sales. This is very similar to the comments made on the previous point. Sales attributable to Fox’s five largest OEM customers accounted for approximately 23% of its sales in 2022. Ford has also recently represented 11% of Fox sales during 2019.

U.S. policies related to global trade and tariffs could have a material effect on Fox’s results. While Fox was barely affected by the trade tariffs imposed on steel and aluminum during 2018, future tariffs may negatively impact Fox’s supply chain costs, possibly lowering the company’s margins.

Conclusion

As you may have noticed, we skipped the valuation section of this article. This is because we believe FOXF 0.00%↑ is not up to par, in terms of quality, with the types of businesses we seek to own at Moonlight Capital. Fox has many things going for it, and we wouldn’t be surprised if in 3 years we are covering the company as one of our mistakes of omission. However, at the time being, this business doesn’t give us the confidence necessary to consider building a position on it.

Below are some of the main reasons which led to this conclusion:

Concerns about loss of experienced management team:

The duo that led Fox’s success, namely Larry Enterline and Zvi Glasman, have recently left the company. Although the company has delivered outstanding results since 2020, these have mostly been driven by the tailwinds created by the pandemic, which drove outsized demand for the markets Fox covers.

Most executives also have very low levels of skin in the game for our standards and the company has experienced very high turnover at the CFO level.

Love the Bike Business, but Auto is much more competitive and fragmented

As we’ve already covered, the bike suspension market is an effective duopoly dominated by Fox and RockShox. The Fox brand is extremely well-regarded in the bike market after about two decades of dominating the premium segment. However, the auto industry is much more competitive, with very capable players such as King, Icon and Bilstein to name a few. We believe Fox’s position is not as strong in Powered Vehicles.

We find it hard for Fox to find relevant success in the on-road market

One of Fox’s goals is to eventually expand into the on-road market to further grow its sales. However, we believe Fox will struggle to accomplish this feat, as it is hard to justify Fox products’ price tag if you’re mostly driving on paved roads. For example, an entry-level Fox 2.0 could improve the handling of a daily driver, but you’d only really begin to see the performance gains at medium-to-high shaft speeds in off-road situations where you’re using a lot of the shock travel.

This is a difficulty Fox has already stumbled upon in their attempt to expand into the commercial truck market. It has found some success in selling suspension products for owner/operator commercial truck vehicles, however they’re struggling to sell products to larger-fleet operators, as management has seen these customers are reluctant to spend that much money on a premium shock.

Not only that, but Fox’s reputation has, in its majority, been built off the road, while other players such as Bilstein have a proven track record in on-road settings at a significantly lower price.

Not too Optimistic on the prospects of the upfitting business

Finally, we are not big fans of the upfitting businesses (SCA, Tuscany and Outside Van). We believe the upfitting business has mostly benefited from the recent periods where “normal” truck alternatives such as basic raptors where hard to find, and people had no choice but to buy Fox’s more expensive trucks. We would like to see how the upfitting business, mostly SCA, performs in a more normal environment before considering it a good acquisition from the Fox team.

Closing

And that’s all from me today! I hope you found this post valuable, and if you did, I would greatly appreciate it if you could share it in the button below.

If you are interested in long-term investing & market psychology, you can subscribe to this newsletter, where you’ll receive articles sharing valuable insights on these topics for free.

And you can also follow me on Twitter, where I share short-form content on a daily basis, including a weekly thread and quotes from great investors.

Very good couple of articles of $FOXF

It seems that I am a much more by the numbers investor than you.

I have qualitative dealbreakers, but I can give an opportunity to a new management if the numbers add up, maybe I have a more pragmatic approach.

Have you looked again at this name after the huge tumble it took after the last earning release?

Given your more qualitative approach I would assume that the Marucci acquisition is another dealbreaker and i concede that it's a very strange mixture with the rest of their operations. But the company has solid margins and it's a CODI name as FOXF itself.

I am not a stockholder, but I am starting to see value even under conservative assumptions.

Would be great to get your take with the new added information.

Thanks!

Thanks for a brilliant deep dive!